INSURANCE INFORMATION INSTITUTE Florida Press Office: (813) 480-6446, lynnem@iii.org

New York Press Office: (212) 346-5500, media@iii.org

TAMPA, FL, July 28, 2011 — Insurance premiums are rising for homes, vehicles and businesses—and policyholders want to know why. The answer is straightforward: claims payouts have been steadily rising in Florida and insurance rates reflect this trend. There are multiple factors driving up claims, including a few insurance mandates unique to Florida, fraud and economic conditions, according to the Insurance Information Institute (I.I.I.).

Insurers cannot charge any price they desire for insurance. State rating laws require that certain legal standards be met, and those laws also dictate a profit margin. Florida insurance regulators review and approve rates to make sure they are adequate, reasonable and not unfairly discriminatory. Additionally, rate increases for insurance reflect loss trends, and insurance companies charge premiums to align with these trends.

For property insurance, rates have to be sufficient to handle anticipated claims relative to each individual company’s exposure to calamities, such as kitchen fires, thefts and burst water pipes, and its exposure to catastrophes like hurricanes and tornadoes. For auto insurance, rates are set based upon losses related to the company’s own experience with payouts for car crashes, including vehicle repair and medical treatments for injured drivers and passengers.

Because so much attention on property insurance in Florida is focused on the state’s vulnerability to hurricane damage, there is confusion over why rates would rise when there has not been a hurricane landfall since 2005.

Preparing for the likelihood of another major storm is only part of the cost, said the I.I.I. In the nearly six years since Hurricane Wilma, it is the “everyday claims” and reopened and new claims from past storms that have caused losses to skyrocket by 80 percent in five years (see chart). Insurers are asking for rate increases and bringing the required legal documentation to show these increasing claims payouts. “Rate requests are based not only on projections of future claims costs for catastrophic natural disasters, but on claims already paid out,” said Lynne McChristian, Florida representative for the I.I.I.

One of the biggest drivers of increasing claims payouts for property insurance was a legislative change made in 2005 that required insurers to pay full replacement cost for home repair upfront. Florida was the only state with such a provision, and it often caused insurers to pay more for repairs than what the actual costs might be because the check was written based on a repair estimate rather than the actual costs of the completed work. In other states, insurers first pay homeowners who have purchased a replacement cost policy an amount equal to actual cash value and pay the remainder as repair work is completed or after a damaged item is replaced.

Tying the payouts to actual receipts is a proven measure for keeping costs fair and equitable. Beginning this year, legislation was enacted to realign Florida to the practice of paying actual cash value for structural repairs as all other states do, although full replacement costs must be paid upfront for the contents of a home.

Another cost factor leading to skyrocketing property insurance claims payouts was a provision that allowed people five years to file a claim for hurricane damage. In other states, there is typically a one year claims-filing deadline, though states have sometimes extended the deadline on an annual basis following major storms. Legislation passed this year limits the claim timeframe to three years in Florida.

According to data from ISO, non-catastrophe claims averaged about $450 per policy through the end of 2010, as compared to $250 per policy in 2007. These claims costs are increasing at 17 percent per year, making today’s projected costs about $500 per policy for “everyday” claims, which are those not associated with natural disasters. It includes costs related to paying sinkhole claims.

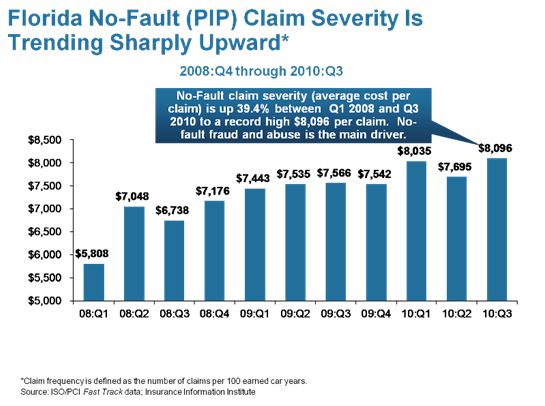

For automobile insurance, insurers are paying out more for each claim while the volume of claims is increasing. Claim severity is defined as the size of the loss, and the chart below shows that the average cost per claim increased by nearly 40 percent in less than three years.

In early 2008, the average claim for an auto accident was $5,808. By the third quarter of 2010, the average cost was $8,096

per claim. Florida is one of 12 states with a no-fault law that allows drivers to file a claim for injuries related to a car crash regardless of fault. Also known as Personal Injury Protection, this coverage provides up to $10,000 for medically necessary expenses; however, that $10,000 has become a “dollar target” for dishonest medical providers and attorneys to manipulate at the expense of all insured drivers. The

Florida Division of Insurance Fraud is working aggressively to investigate and prosecute those involved in this type of insurance fraud. The I.I.I. has estimated that Florida drivers paid a “fraud tax” of about $49 per vehicle in 2010, which is expected to climb to nearly $84 per vehicle this year, absent any reforms to stem fraud and abuse.

The I.I.I. has produced a report on No-fault Auto Insurance Trends in Florida and an Overview of the Florida Property Insurance Market.

THE I.I.I. IS A NONPROFIT, COMMUNICATIONS ORGANIZATION SUPPORTED BY THE INSURANCE INDUSTRY.

Insurance Information Institute, 4775 E. Fowler Avenue, Tampa, FL 33617, (813) 480-6446 | www.insuringflorida.org| www.iii.org