A yard sale is a great way to clean out your home, make a little money and do some good for the environment by providing a second life for your possessions. But your enterprise could get expensive if someone gets hurt on your property and decides to sue.

Here are some steps to keep your yard sale customers safe:

- Repair loose railings and cracked concrete.

- Place sale items so that there is enough space to move about without tripping.

- Don’t place items too close to stairs and ledges where people could fall.

- Keep sharp objects such as knives and scissors out of the reach of children.

- Do not sell unsafe, hazardous, or recalled items.

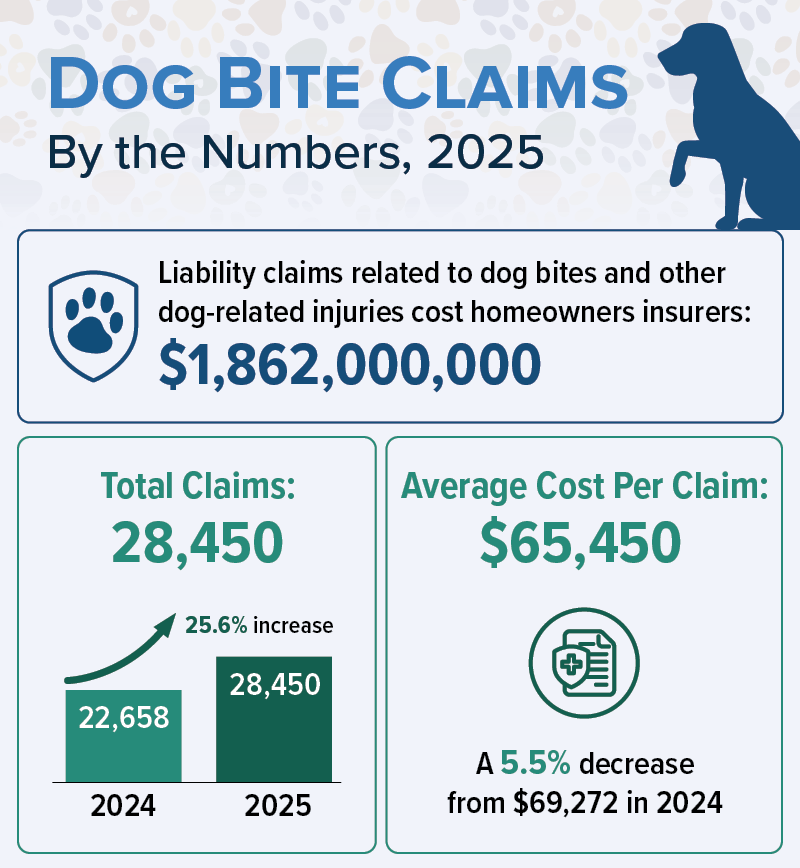

- Keep your pets indoors during the sale, both for their safety and to avoid someone getting hurt. Some dogs can become very protective when there are strangers on their property.

- If someone does get injured, get him or her immediate medical attention.

In addition to taking safety precautions, protect yourself by making sure you have adequate insurance coverage for the type of sale you are holding:

- One time yard sale – Events for the sole purpose of selling unwanted personal items are generally covered under a standard homeowners or renters policy. However, it is important to have enough liability coverage, so be sure to check with your insurance professional.

- Frequent yard sales – If you have frequent yard sales, it is a good idea to purchase a separate policy for business liability or an in-home business policy. These policies are available from many homeowners insurance companies and specialty insurers.

- Charity fundraiser – If you are staging a sale to raise money for a charity, you will most likely be covered under your homeowners or renters insurance policy. But you can also contact the charity to see what type of insurance protection they would be willing to extend to you if necessary.

Next steps: Have people over frequently? Read about your social host liability.