INSURANCE INFORMATION INSTITUTE

Florida Press Office: (813) 480-6446, lynnem@iii.org

New York Press Office: (212) 346-5500, media@iii.org

Florida Insurance Council: (850) 459-3012; smiller@flains.org

TAMPA, Florida, July 25, 2013 — If you’ve chosen a high hurricane deductible, you are saving money every year on homeowners insurance. That may be a good strategy when tropical storms remain far from Florida, but it could prove otherwise when a hurricane actually strikes. As the height of hurricane season approaches, the

Insurance Information Institute (I.I.I) and

Florida Insurance Council (FIC) suggest that Floridians review their hurricane deductibles to make sure they understand what that decision will cost them and have a plan to pay for it.

“Because Floridians have had a seven-year reprieve from paying hurricane deductibles, it may be time for some homeowners to revisit decisions they made about covering these deductible costs,” said Lynne McChristian, Florida representative for the I.I.I.

Florida homeowners insurance policies have two deductibles—one for damage from hurricanes and another for damage related to other perils covered under the policy, including non-hurricane windstorms. Deductibles are the amount of a loss paid by a policyholder, and a high deductible always makes annual premiums lower. Paying less for insurance—even a few dollars a year less—seems right when the weather is calm. But high deductibles mean a policyholder takes on the extra risk, and that is not something many people consider. Policyholders should make sure their deductible decisions are affordable.

“Saving money on insurance in the present day sounds smart, yet forgetting what that decision may cost you if a hurricane strikes is risky,” McChristian said. “It is a good idea to match up the premium cost savings of various hurricane deductible options with the out-of-pocket costs you will have to bear if your home is damaged and requires costly repairs.”

Sam Miller, executive vice president of the Florida Insurance Council, explains, “Weighing the cost of the hurricane deductible options allows you to be better able to judge the long-term financial implications of your decision.”

In Florida, homes with insured values of less than $100,000 have either a flat dollar amount hurricane deductible, starting at $500, or a percentage deductible that the homeowner chooses; homes insured for $100,000 or more typically have percentage hurricane deductibles that start at 2 percent; homeowners also may choose higher hurricane deductibles such as 5 percent or 10 percent. Remember, these percentages are based on the insured value of the entire home, NOT the loss amount. Insured value, in turn, is based on the costs of rebuilding your home after a disaster. It is different from the estimated real estate market value of your home.

HURRICANE DEDUCTIBLE OPTIONS INTRODUCED AFTER ANDREW

Following the devastation caused by Hurricane Andrew in 1992, the Florida Legislature introduced the concept of a separate hurricane deductible; by 1998, all property insurers were required to offer them. Hurricane deductibles have helped to make more private insurance available in coastal areas at a lower price. Additionally, people who select a high deductible have an incentive to mitigate hurricane damage by protecting property from high winds, so their chances of severe damage are diminished.

Eighteen states and the District of Columbia have two different types of deductibles: one for hurricanes or wind damage and one for everything else. An “all other perils” deductible is typically a flat dollar amount of $500, $1,000 or $2,000, and it covers damage from calamities such as fire, lightning or if a pipe bursts inside your home. The separate deductible for hurricanes is a percentage of the insured value of a home.

HOW A HURRICANE DEDUCTIBLE WORKS

Homeowners get a premium credit for taking on the extra risk associated with a hurricane deductible and, ideally, some of the credit could be saved up to pay the hurricane deductible. Understandably, this is not something everyone can afford to do—and those are the individuals most at risk if they choose a hurricane deductible that is higher than they can in reality pay.

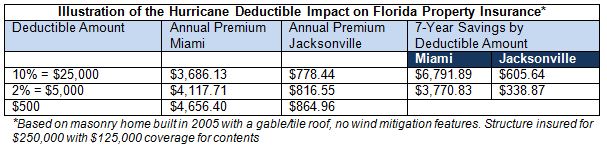

A policyholder who has chosen a 10 percent hurricane deductible pays less for property insurance than someone who chose a 2 percent deductible—but paying less for insurance now means paying five times more in out-of-pocket costs if a hurricane strikes the property.

Consider a home insured for $250,000 with a 2 percent hurricane deductible. If a hurricane strikes, the 2 percent hurricane deductible means an out-of-pocket cost of $5,000. As the illustration below demonstrates, the savings with a 2 percent deductible have added up over the past seven hurricane-free years in Florida, but the impact of the savings is greater in areas where the annual premium is highest. It would require decades without hurricanes for the premium savings from a 10 percent hurricane deductible to reach economic balance for a homeowner.

Policyholders are alerted to the hurricane deductible in multiple places within the insurance contract.

- In Florida, there is a message in 18-point boldface type at the front of the policy as prescribed by law.

- The exact dollar amount of the hurricane deductible is itemized on the policy declaration page.

- A one-page insert in the policy packet outlines deductible options and the weather conditions necessary before they apply.

Because most insurers allow deductible options to be revised only before a policy is renewed, a change you make today may not take immediate effect. The I.I.I. suggests policyholders contact their insurance professional for an annual review of insurance coverage and deductible options to make sure the decisions made continue to be the best ones for their personal financial situations.

RELATED LINKS

The I.I.I. has a full library of educational videos on its

You Tube Channel. Information about I.I.I. mobile apps can be found

here.

THE I.I.I. IS A NONPROFIT, COMMUNICATIONS ORGANIZATION SUPPORTED BY THE INSURANCE INDUSTRY.

Insurance Information Institute, 4775 E. Fowler Avenue, Tampa, FL 33617, (813) 480-6446