MEMBERSHIP

AMPLIFY

EN ESPAÑOL

Connect With Us

- Popular search terms

- Automobile

- Home + Renters

- Claims

- Fraud

- Hurricane

- Popular Topics

- Automobile

- Home + Renters

- The Basics

- Disaster + Preparation

- Life Insurance

The basic personal auto insurance mandated by most U.S. states provides some financial protection if you or another driver using your car causes an accident that damages someone else’s car or property, injures someone or both.

But to make the best decisions about purchasing other types of auto insurance coverage you might need, you will want to understand what’s covered, what’s not covered and what’s optional. In addition to understanding types of coverage, you will also want to consider coverage amounts.

Why? Because state-required minimums may not cover the costs of a serious accident, so it’s worth considering purchasing higher levels of coverage.

Here’s a rundown of the types of coverage available. While some are required, others are optional. All are priced individually to let you customize coverage amounts to suit your exact needs and budget.

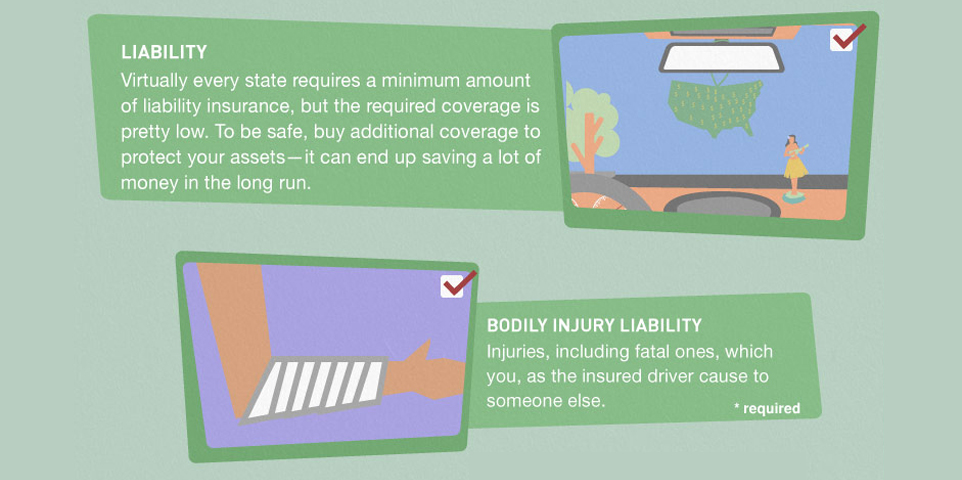

Nearly all states and Washington, D.C., require vehicle owners to carry the following auto liability coverages:

Even if these types of coverage are optional in your state, consider adding them to your policy for greater financial protection.

While legally mandated auto liability insurance covers the cost of damages to other vehicles that you cause while driving, it does not cover damage to your own car. Optional collision and comprehensive coverages are typically part of a full-coverage policy.

If you lease or finance your vehicle, auto dealers or leasing companies will likely require you to purchase collision and comprehensive. But keep in mind that collision and comprehensive only cover the market value of your car, not what you paid for it—and new cars depreciate quickly. If your car is totaled or stolen, there may be a “gap” between what you owe on the vehicle and your insurance coverage. To cover this, you may want to look into purchasing gap insurance to pay the difference.

Your auto policy will cover you and other family members on your policy, whether driving your insured car or someone else’s car with permission. Your policy also provides coverage if someone not on your policy is driving your car with your consent.

Your personal auto policy only covers personal driving, whether you are commuting to work, running errands or taking a road trip. Your personal auto policy, however, will not provide coverage if you use your car for commercial purposes—for instance, if you deliver pizzas or operate a delivery service.

Note, too, that personal auto insurance will generally not provide coverage if you use your vehicle to provide transportation to others through a ride-sharing service such as Uber or Lyft. Some auto insurers, however, offer supplemental insurance products (at additional cost) that extend coverage for vehicle owners providing ride-sharing services.

Learn More: Check out this handy infographic on the types of required and optional drivers insurance coverages.