Defining legal system abuse

Triple-I defines Legal System Abuse as policyholder or plaintiff attorney practices which increase costs and time to settle insurance claims. While litigation is considered a policyholder’s last resort, legal system abuse exploits litigation when a disputed claim could have been resolved without judicial intervention. Legal system abuse contributes to higher costs for insurance operations and policyholder pricing.

Four big issues contribute to legal system abuse in the U.S., the biggest cost driver of social inflation, the Insurance Information Institute has found. Legal system abuse refers to disputed insurance claims which could have been resolved without litigation.

- Third-Party Litigation Funding (TPLF): Without any transparency or direct ties to litigated cases, institutional investors and even sovereign nations contribute significant amounts of capital toward litigation suits for the sole intent of making a profit.

- Plaintiff Attorney Advertising “The Billboard Effect”: Through erosion of judicial standards and authority, plaintiff attorneys spend billions of dollars annually on advertising, hinting at a financial windfall for policyholders who retain their services.

- Increasing Plaintiff Attorney Contingency Fees: Insured claimants receive smaller portions of total settlements as attorneys and third-party litigation funders look to profit even more.

- Eroding Caps on Damages: Settlements and case damage awards increased 27.5 percent on average between 2010 and 2019, the U.S. Chamber Institute for Legal Reform determined, due to little or no limit on the amount of damages in the U.S. judicial system.

The consequences of legal system abuse, and the social inflation it causes, are significant. Higher costs for the insurance ecosystem increase the price of insurance coverage for all consumers and businesses.

What is the impact of social inflation?

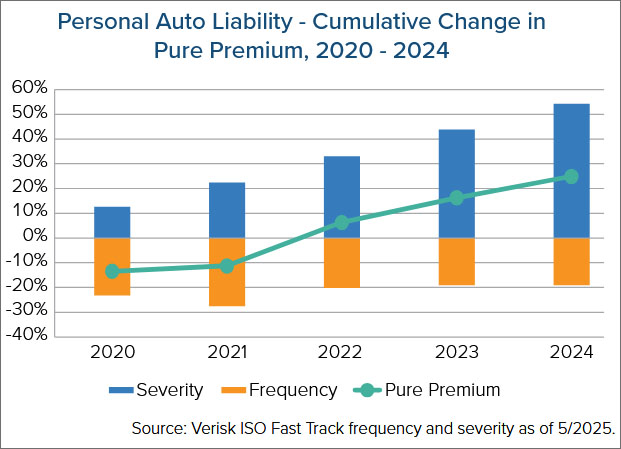

Social inflation drives higher insurer claim payouts and loss ratios. Ultimately, policyholders pay more for coverage. A simple way to think about social inflation and its components is to compare the impact of these factors on claims losses over time with growth in an inflation measure like the Consumer Price Index (CPI). The insurance lines that tend to bear the brunt are commercial auto, professional liability, product liability, and directors and officers liability. However, evidence indicates that pressure is mounting on private passenger automobile insurance, too.

Insights on social inflation

While social inflation remains hard to predict and mitigate, it is crucial to understand the factors at play and the risks to all stakeholders. We’ll continue developing research and curating thought leadership resources to raise awareness. Follow our content here and on the Triple-I Blog to stay abreast of this critical issue.

- Florida Insurance Costs 14.5% Lower Than Without Reforms, Report Finds

- Triple-I Blog: Florida Governor Touts Auto Insurance Rebates, Tort Reform Success

- Report: Review of Motor Vehicle Tort Cases Across the Federal And State Civil Courts and Video: Motor Vehicle Civil Tort Report

- Litigation Reform Works: Florida Auto Insurance Premium Rates Declining

- A Consumer Guide: How legal system abuse impacts you

- Forget ‘Social Inflation’; Think ‘Legal System Abuse‘

- Take a look at our latest issue briefs focused on Florida, Georgia and Louisiana insurance markets which discuss how excessive claims litigation and attorney involvement drive up costs, and, ultimately, premium rates.

- Public Comment from Triple-I Chief Insurance Officer Dale Porfilio, Public Comment on Proposed Amendments to Section 202.67 and Section 207.38 of the Uniform Civil Rules for the New York Supreme Court and County Court (22 NYCRR §§ 202.67 & 207.38) Relating to Litigation Financing Agreements.

- An op-ed from Triple-I CEO Sean Kevelighan, Who’s Financing Legal System Abuse? Louisianans Need to Know.

- Here’s our latest article on insurance premium rates across the U.S., Triple-I: Managing Risk Effectively Protects Policyholders.

- For background on the Florida legal system, read our latest article Legalized Fraud in Florida: Stormy Waters Ahead, guest blog by Matthew Scarfone, Esq., Some Potential Sunshine for Florida’s Property Insurance Market and download our infographic, Florida Property Insurance Market (June 2023).

- Go more in-depth with our latest issues brief, Legal System Abuse: State of the Risk .

- Take a deeper dive with our latest research, Commercial Auto: Trends and Insights.

- Triple-I launches campaign to highlight challenges to insurance affordability in Georgia.

- Testimony by Triple-I Chief Insurance Officer and IRC President Dale Porfilio before Louisiana House Insurance Committee.

- Learn what can be done to Stop Legal System Abuse.

- What Independent Agents Need to Know About Legal System Abuse

- Increasing Inflation on Auto Liability Insurance – Impact as of Year-End 2023