(Percentage distribution)

MEMBERSHIP

AMPLIFY

EN ESPAÑOL

Connect With Us

- Popular search terms

- Automobile

- Home + Renters

- Claims

- Fraud

- Hurricane

- Popular Topics

- Automobile

- Home + Renters

- The Basics

- Disaster + Preparation

- Life Insurance

(Percentage distribution)

Source: © 2017 Munich Re, Geo Risks Research, NatCatSERVICE. As of February 2017.

(Number of relevant events by peril)

Source: © 2019 Munich Re, Geo Risks Research, NatCatSERVICE. As of March 2019.

(Number of relevant events by peril)

Source: © 2018 Munich Re, Geo Risks Research, NatCatSERVICE. As of January 2018.

Source: © 2017 Munich Re, Geo Risks Research, NatCatSERVICE. As of February 2017.

Source: © 2019 Munich Re, Geo Risks Research, NatCatSERVICE. As of March 2019.

Source: © 2018 Munich Re, Geo Risks Research, NatCatSERVICE. As of January 2018.

Source: © 2017 Munich Re, Geo Risks Research, NatCatSERVICE. As of February 2017.

(Percentage distribution)

Source: © 2019 Munich Re, Geo Risks Research, NatCatSERVICE. As of March 2019.

(Percentage distribution)

Source: © 2018 Munich Re, Geo Risks Research, NatCatSERVICE. As of January 2018.

(Percentage distribution)

Source: © 2017 Munich Re, Geo Risks Research, NatCatSERVICE. As of February 2017.

($ billions)

Source: NYSE Euronext; Securities Industry and Financial Markets Association.

Source: Swiss Re, sigma, No. 3/2008.

TOTAL AUTO PREMIUMS BY SECTOR, 2007

Source: National Association of Insurance Commissioners (NAIC) Annual Statement Database, via Highline Data, LLC. Copyrighted information. No portion of this work may be copied or redistributed without the express written permission of Highline Data, LLC.

PERCENT CHANGE FROM PRIOR YEAR, NET PREMIUMS WRITTEN, PRIVATE PASSENGER AUTO, 1999-2007

Source: National Association of Insurance Commissioners (NAIC) Annual Statement Database, via Highline Data, LLC. Copyrighted information. No portion of this work may be copied or redistributed without the express written permission of Highline Data, LLC.

WHERE THE REVENUE DOLLAR GOES, 2007

(Premiums and investments)

POPULATION GROWTH PROJECTIONS FOR HURRICANE EXPOSED STATES, 2000-2030

(000)

Source: U.S. Department of Commerce, Census Bureau.

WORLD LIFE AND NONLIFE INSURANCE PREMIUMS, 2007

Source: Swiss Re, sigma, No. 3/2008.

ASSETS OF HEDGE FUNDS, 1950-2008 (1)

($ billions)

(1) As of January.

Source: Hennessee Group LLC.

SEPARATELY MANAGED ACCOUNTS INDUSTRY ASSETS UNDER MANAGEMENT, 2003-2007

($ billions)

Source: Money Management Institute, Dover Financial Research.

TOTAL RECEIVABLES OUTSTANDING AT FINANCE COMPANIES BY CATEGORY, 2003 AND 2007 (1)

(1) Includes finance company subsidiaries of bank holding companies but not of retailers and banks. Includes owned receivables (carried on the balance sheet of the institution) and managed receivables (outstanding balances of pools upon which securities have been issued; these balances are no longer carried on the balance sheets of the loan originator).

Source: Board of Governors of the Federal Reserve System.

($ billions)

(1) Represents homeowners’ cash withdrawals from home mortgage refinance transactions. Includes prime conventional loans only and is net of retirement of outstanding second mortgages.

(2) Estimated.

Source: Freddie Mac.

(1) HECMs are federally insured reverse mortgage products.

(2) Through June 30, 2008; fiscal year ends September 30.

Source: National Reverse Mortgage Lenders Association.

(Percent)

Source: U.S. Department of Commerce, Census Bureau, Housing Vacancy Survey.

HOME OWNERSHIP RATES, 1900-2007

Source: U.S. Department of Commerce, U.S. Census Bureau, Census of Housing.

(1) Information technology expense per total company full-time employee.

Source: Ward Group.

Source: Ward Group.

(1) Information technology expense per total company full-time employee.

Source: Ward Group.

IT SPENDING AS A PERCENT OF TOTAL PREMIUMS WRITTEN BY LIFE, ANNUITIES AND HEALTH INSURANCE COMPANIES, 2002-2006

Source: Ward Group.

(1) Automated Clearing House.

Source: Board of Governors of the Federal Reserve System.

DEBT GROWTH BY SECTOR, 1998-2007 (Percent change from prior year)

Source: Board of Governors of the Federal Reserve System, June 5, 2008.

ASSETS OF PRIVATE PENSION FUNDS, 1945-2007

($ billions, end of year)

Source: Board of Governors of the Federal Reserve System, June 5, 2008.

($ billions)

Source: GC Securities, a division of MMC Securities Corp., a U.S. registered broker-dealer, member FINRA/SIPC, and Guy Carpenter.

($ billions)

Source: GC Securities, a division of MMC Securities Corp., a U.S. registered broker-dealer, member FINRA/SIPC, and Guy Carpenter.

GROWTH IN U.S. PREMIUMS, PROPERTY/CASUALTY AND LIFE/HEALTH INSURANCE, 1998-2007

(Percent change from prior year)

(1) Net premiums written, excluding state funds.

(2) Premiums and annuity considerations for life/health insurance companies. Includes deposit-type funds beginning in 2001.

Source: National Association of Insurance Commissioners (NAIC) Annual Statement Database, via Highline Data, LLC. Copyrighted information. No portion of this work may be copied or redistributed without the express written permission of Highline Data, LLC.

PREMIUMS BY TYPE OF INSURER, 2007 (1)

(1) Gross direct premiums. Total premiums for 2007 were $1,580 billion.

(2) Blue Cross/Blue Shield, HMOs and hospital, medical and dental indemnity.

Source: National Association of Insurance Commissioners. Reprinted with permission. Further reprint or distribution strictly prohibited without written permission of NAIC

PREMIUMS BY TYPE OF INSURER, 2007 (1)

(1) Gross direct premiums. Total premiums for 2007 were $1,580 billion.

(2) Blue Cross/Blue Shield, HMOs and hospital, medical and dental indemnity.

Source: National Association of Insurance Commissioners. Reprinted with permission. Further reprint or distribution strictly prohibited without written permission of NAIC

THE NATION'S HEALTHCARE DOLLAR: 2006 WHERE IT COMES FROM (1)

(1) Does not add to 100 percent due to rounding.

(2) State Children’s Health Insurance Program.

Source: Centers for Medicare and Medicaid Services, Office of the Actuary.

NATIONAL HEALTHCARE EXPENDITURES, AVERAGE ANNUAL PERCENT GROWTH FROM PRIOR YEAR, 1993-2017

(1) Average annual growth from 1970 through 1993; marks the beginning of the shift to managed care.

(2) Projected.

Source: Centers for Medicare and Medicaid Services, Office of the Actuary.

U.S. INDIVIDUAL LIFE MARKET SHARE BY DISTRIBUTION CHANNEL, 1999-2007

(Based on first year collected premium)

(1) Includes career, multiline exclusive and home service agents.

(2) Includes brokers and personal producing general agents.

(3) Includes stockbrokers, financial institution, worksite and other channels.

(4) Estimate.

Source: LIMRA’s U.S. Individual Life Insurance Sales Studies, LIMRA estimates.

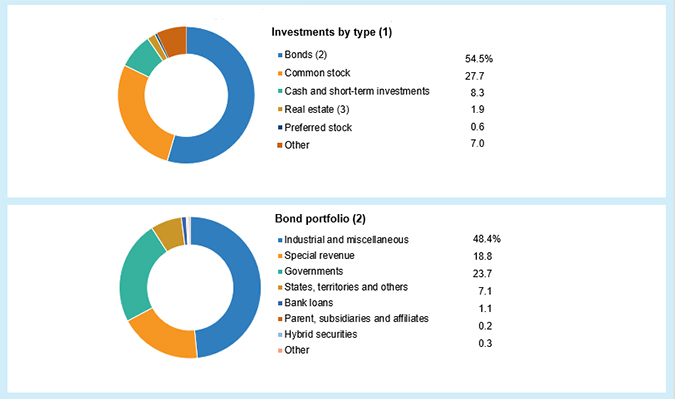

INVESTMENTS, LIFE/HEALTH INSURERS, BOND PORTFOLIO, 2003 AND 2007

Source: National Association of Insurance Commissioners (NAIC) Annual Statement Database, via Highline Data, LLC. Copyrighted information. No portion of this work may be copied or redistributed without the express written permission of Highline Data, LLC.

SALES OF INDIVIDUAL ANNUITIES BY DISTRIBUTION CHANNELS, 2003 AND 2007 (1)

(1) Preliminary.

Source: LIMRA International.

WHERE THE UNDERWRITING DOLLAR GOES, PROPERTY/CASUALTY INSURANCE, ALL LINES, 2007

Source: National Association of Insurance Commissioners (NAIC) Annual Statement Database, via Highline Data, LLC. Copyrighted information. No portion of this work may be copied or redistributed without the express written permission of Highline Data, LLC.

PERCENT CHANGE FROM PRIOR YEAR, NET PREMIUMS WRITTEN, P/C INSURANCE, 1975-2007 (1)

(1) Excludes state funds.

Source: ISO.

OPERATING RESULTS, PROPERTY/CASUALTY INSURANCE, 1998-2007 (1)

($ billions)

(1) Excludes state funds.

(2) Net underwriting gain/loss plus net investment income.

Source: National Association of Insurance Commissioners (NAIC) Annual Statement Database, via Highline Data, LLC. Copyrighted information. No portion of this work may be copied or redistributed without the express written permission of Highline Data, LLC.

PERCENT CHANGE FROM PRIOR YEAR, NET PREMIUMS WRITTEN AND POLICYHOLDERS' SURPLUS, P/C INSURANCE, 1999-2007 (1)

(1) After reinsurance transactions, excluding state funds.

Source: National Association of Insurance Commissioners (NAIC) Annual Statement Database, via Highline Data, LLC. Copyrighted information. No portion of this work may be copied or redistributed without the express written permission of Highline Data, LLC.

PROPERTY/CASUALTY INSURANCE COMBINED RATIO, 1975-2007 (1)

(1) Excluding state funds and residual markets.

Source: ISO.

(1) Cash and invested assets, as of December 31, 2007.

(2) Long-term bonds with maturity dates over one year.

Source: National Association of Insurance Commissioners (NAIC) Annual Statement Database, via Highline Data, LLC. Copyrighted information. No portion of this work may be copied or redistributed without the express written permission of Highline Data, LLC.

TOTAL GROSS SURPLUS LINES PREMIUMS WRITTEN, 2003-2007

($ billions)

Source: 2005 to 2007 premiums from Business Insurance, September 8, 2008; earlier premiums from other issues.

MARKET SHARE TRENDS BY SIZE OF INSURER, 1987-2007 (1)

(1) Based on net premiums written, excluding state funds.

Source: ISO.

($ billions)

(1) After reinsurance transactions, excluding state funds.

(2) Before reinsurance transactions, excluding state funds. May not match total premiums shown elsewhere in this book because of the use of different exhibits from Highline Data LLC.

(3) Includes international and miscellaneous coverages.

(4) Premiums from certain insurers that write health insurance but file financial statements with state regulators on a property/casualty basis.

(5) Only includes nonproportional reinsurance, an arrangement in which a reinsurer makes payments to an insurer whose losses exceed a predetermined amount.

(6) Coverages protecting against legal liability resulting from negligence, carelessness, or failure to act.

Source: National Association of Insurance Commissioners (NAIC) Annual Statement Database, via Highline Data, LLC. Copyrighted information. No portion of this work may be copied or redistributed without the express written permission of Highline Data, LLC.

Source: National Association of Insurance Commissioners (NAIC) Annual Statement Database, via Highline Data, LLC. Copyrighted information. No portion of this work may be copied or redistributed without the express written permission of Highline Data, LLC.

WORKERS COMPENSATION MEDICAL COSTS, 1998-2007

(1) Based on states where the National Council on Compensation Insurance provides ratemaking services. Represents costs for injuries that resulted in time off from work. Data for 2007 is preliminary.

Source: U.S. Bureau of Labor Statistics; National Council on Compensation Insurance.

(2007 $ billions)

(1) Catastrophes are all events causing direct insured losses to property of $25 million or more in 2007 dollars. Adjusted for inflation by ISO.

(2) Includes hurricanes and tropical storms.

(3) Excludes snow.

(4) Includes other geologic events such as volcanic eruptions and other earth movement.

(5) Does not include flood damage covered by the federally administered National Flood Insurance Program.

(6) Includes wildland fires.

Source: ISO's Property Claim Services unit (PCS).

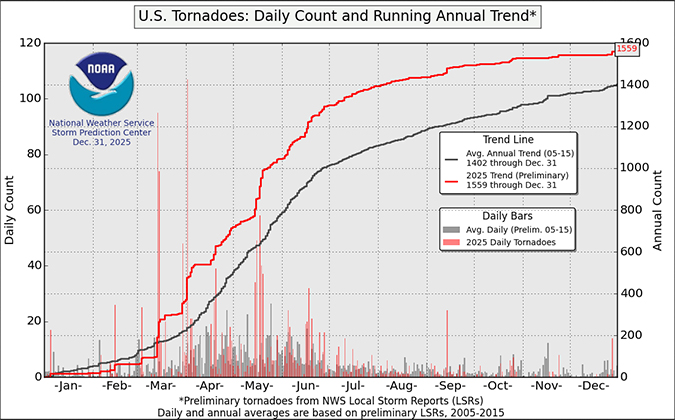

NUMBER OF TORNADOES AND RELATED DEATHS PER MONTH, 2007

Source: U.S. Department of Commerce, Storm Prediction Center, National Weather Service.

(1) Reported to local fire departments.

Source: National Fire Protection Association.

LIGHTNING INCIDENTS BY MONTH, 2002-2005 (1)

(1) Reported to local fire departments.

Source: National Fire Protection Association.

MOTOR VEHICLE DEATHS BY ACTIVITY OF PERSON KILLED, 2007

(1) Includes other nonoccupants.

Source: U.S. Department of Transportation, National Highway Traffic Safety Administration.

MOTOR VEHICLE DEATHS PER 100,000 PERSONS BY AGE, 2007

Source: Insurance Institute for Highway Safety.

INSURANCE EXPENDITURES AS A PERCENTAGE OF TOTAL HOUSEHOLD SPENDING, 2007

Source: U.S. Department of Labor, Bureau of Labor Statistics.

(Percent)

(1) Loss experience in the past 5 years.

Source: 2007 Limits of Liability Report, © Marsh Inc. 2007.

U.S. AVERAGE EXCESS LIABILITY LIMITS RELATIVE TO LOSS EXPERIENCE, 2003-2007

(Average limits purchased, $ millions)

(1) Loss experience in the past 5 years.

Source: 2007 Limits of Liability Report, © Marsh Inc. 2007.

DIRECTORS AND OFFICERS LIABILITY CLAIMS BY TYPE OF CLAIMANT IN THE UNITED STATES, 1997-2007

NA=Not applicable.

Source: 2007 Directors and Officers Liability Survey, Tillinghast-Towers Perrin.

MEDIAN (1) AND AVERAGE PERSONAL INJURY JURY AWARDS, 2000 AND 2006 ($000)

(1) Represents the midpoint jury award. Half of awards are above the median and half are below.

Source: Reprinted with permission from Current Award Trends in Personal Injury. Copyright 2008 by LRP Publications, 747 Dresher Road, P.O. Box 980, Horsham, PA 19044-0980. All rights reserved.

($ billions, excludes state funds)

(1) Includes deposit-type funds beginning in 2001.

Source: National Association of Insurance Commissioners (NAIC) Annual Statement Database, via Highline Data, LLC. Copyrighted information. No portion of this work may be copied or redistributed without the express written permission of Highline Data, LLC.

ASSETS OF FINANCIAL SERVICES SECTORS, 2007; & FINANCIAL SERVICES EMPLOYMENT BY INDUSTRY, 2007

ASSETS OF FINANCIAL SERVICES SECTORS 2003, 2007

($ billions)

NUMBER OF ANNOUNCED FINANCIAL SERVICES MERGERS AND ACQUISITIONS, 2003-2007

Source: SNL Financial LC.

(000)

Source: U.S. Department of Labor, Bureau of Labor Statistics.

GROSS DOMESTIC PRODUCT OF FINANCIAL SERVICES, SHARES BY COMPONENT, INCLUDING REAL ESTATE, 2006

Source: U.S. Department of Commerce, Bureau of Economic Analysis.

GROSS DOMESTIC PRODUCT OF FINANCIAL SERVICES, SHARES BY COMPONENT, EXCLUDING REAL ESTATE, 2006

Source: U.S. Department of Commerce, Bureau of Economic Analysis.

GROSS NATIONAL SAVINGS, 1940-2007 ($ billions)

(1) Includes individuals (including proprietors and partnerships), nonprofit institutions primarily serving individuals, life insurance carriers and miscellaneous entities.

Source: U.S. Department of Commerce, Bureau of Economic Analysis.

HOLDINGS OF U.S. CORPORATE EQUITIES, 2007 (1)

(1) Market value, end of year; excludes open-end mutual fund shares.

(2) Holdings of U.S. issues by foreign residents.

Source: Board of Governors of the Federal Reserve System, June 5, 2008.

(Percent of all U.S. households)

Source: Investment Company Institute; U.S. Department of Commerce, Bureau of the Census.

NUMBER OF AND DOLLARS INVESTED IN 529 PLAN ACCOUNTS, 2003-2007

Source: National Association of State Treasurers.

IDENTITY THEFT AND FRAUD COMPLAINTS, 2005-2007 (1)

(1) Percentages are based on the total number of identity theft and fraud complaints by calendar year. These figures exclude national "Do Not Call" registry complaints.

Source: Federal Trade Commission.

($ trillions, end of year)

(1) Data for 2003, 2005, 2006 and 2007 are estimates.

Source: Investment Company Institute.

RETIREMENT FUNDS ASSET MIX, 2007

Source: Securities Industry and Financial Markets Association.

(000)

(1) Deferred status refers to individuals eligible for future payments.

(2) Payees are retired participants or their beneficiaries receiving payments.

Source: Pension Benefit Guaranty Corporation.

IRA MARKET SHARES BY HOLDER, 2003 AND 2007

Source: Board of Governors of the Federal Reserve System, June 5, 2008.

Source: Based on data from Investment Company Institute: Holden, Sarah, James Duvall, and Elena Barone Chism. 2021. “The Economics of Providing 401(k) Plans: Services, Fees, and Expenses, 2020.” ICI Research Perspective 27, no. 6 (June). Available at www.ici.org/files/2021/ per27-06.pdf.

SALES OF INDIVIDUAL ANNUITIES BY DISTRIBUTION CHANNELS, 2003 AND 2007 (1)

(1) Preliminary.

Source: LIMRA International.

VARIABLE ANNUITY TOTAL SALES BY DISTRIBUTION CHANNEL, 2007 (1)

(1) As of December 31, 2007.

(2) Regulated by the Financial Industry Regulatory Authority.

Source: Morningstar, Inc.

($ billions)

Source: Morningstar, Inc.

MUTUAL FUND RETIREMENT ASSETS BY TYPE OF PLAN, 2007 (1)

($ billions)

(1) Preliminary.

Source: Investment Company Institute.

($ billions)

(1) Estimated.

Source: Bank Insurance and Securities Research Associates (BISRA).

BANK INDIVIDUAL LIFE INSURANCE SALES, 2003-2007

($ millions)

Source: Kehrer-LIMRA.

(1) Based on the responses of banks in the survey that sell insurance products.

Source: 2010 Survey of Banks in Insurance, American Bankers Insurance Association.

(1) Percent of surveyed banks distributing these insurance products.

Source: 2010 Survey of Banks in Insurance, American Bankers Insurance Association.

PREMIUMS BY TYPE OF INSURER, 2007 (1)

(1) Gross direct premiums. Total premiums for 2007 were $1,580 billion.

(2) Blue Cross/Blue Shield, HMOs and hospital, medical and dental indemnity.

Source: National Association of Insurance Commissioners (NAIC). Reprinted with permission. Further reprint or distribution strictly prohibited without written permission of NAIC.

U.S. PROPERTY/CASUALTY AND LIFE/HEALTH INSURANCE PREMIUMS, 2007 (1)

(1) Excluding state funds.

Source: National Association of Insurance Commissioners (NAIC) Annual Statement Database, via Highline Data, LLC. Copyrighted information. No portion of this work may be copied or redistributed without the express written permission of Highline Data, LLC.

TYPES OF BONDS INSURED BY FINANCIAL GUARANTY INSURERS, 2007 (1)

(1) Net par outstanding, December 31, 2007.

Source: Association of Financial Guaranty Insurers.

WORKSITE LIFE INSURANCE COMPANY SALES BY LINE OF BUSINESS, 2007 (1)

(1) Short-term and long-term disability.

Source: East Bridge Consultants.

THE NATION'S HEALTHCARE DOLLAR: 2006 WHERE IT COMES FROM (1)

(1) Does not add to 100 percent due to rounding.

(2) State Children’s Health Insurance Program.

Source: Centers for Medicare and Medicaid Services, Office of the Actuary.

ASSETS OF FDIC-INSURED COMMERCIAL BANKS, 2007

Source: Federal Deposit Insurance Corporation.

CREDIT UNION MEMBERS, 1980-2007

(000)

Source: National Credit Union Administration.

(Percent)

(1) New York Stock Exchange members doing public business.

Source: Securities Industry and Financial Markets Association.

($ billions)

(1) New York Stock Exchange members doing public business.

Source: Securities Industry and Financial Markets Association.

(Percent)

(1) New York Stock Exchange member firms doing public business.

Source: Securities Industry and Financial Markets Association.

ASSET-BACKED SECURITY SOURCES, 2003 AND 2007

(1) Securities of federal mortgage pools backing privately issued collateralized mortgage obligations (CMOs). In CMOs, mortgage principal and interest payments are separated into different payment streams to create bonds that repay capital over differing periods of time.

(2) Mortgages backing privately issued pool securities and CMOs.

(3) Treasury securities accounted for less than 1 percent in 2003.

Source: Board of Governors of the Federal Reserve System, June 5, 2008.

MUTUAL FUND INDUSTRY NET ASSETS BY TYPE OF FUND, 2007; & NUMBER OF MUTUAL FUNDS BY TYPE OF FUND, 2007

Source: Investment Company Institute.

(1) Based on states where the National Council on Compensation Insurance provides ratemaking services. Represents costs for injuries that resulted in time off from work. Data for 2009 are preliminary.

Source: U.S. Bureau of Labor Statistics; National Council on Compensation Insurance.

(1) Represents the midpoint jury award. Half of awards are above the median and half are below.

Source: Thomson Reuters.

Source: National Association of State Treasurers.

Source: Thomson Reuters.

Source: Federal Deposit Insurance Corporation.

($ billions)

(1) As of December 9.

Source: GC Securities and Guy Carpenter & Company, LLC.

(Percent change from prior year)

Source: Board of Governors of the Federal Reserve System, June 10, 2010.

($ billions)

(1) As of December 9.

Source: GC Securities and Guy Carpenter & Company, LLC.

($ billions, end of year)

Source: Board of Governors of the Federal Reserve System, June 10, 2010.

($ trillions, year-end)

(1) Estimated.

Source: Investment Company Institute.

(1) Market value, end of year; excludes open-end mutual fund shares.

(2) Holdings of U.S. issues by foreign residents.

Source: Board of Governors of the Federal Reserve System, June 10, 2010.

(1) Percentages are dollar-weighted averages.

Source: Investment Company Institute.

Source: Board of Governors of the Federal Reserve System, June 10, 2010.

($ billions, end of year)

(1) Preliminary data. Does not include defined benefit plans.

Source: Investment Company Institute.

(1) Securities of federal mortgage pools backing privately issued collateralized mortgage obligations (CMOs). In CMOs, mortgage principal and interest payments are separated into different payment streams to create bonds that repay capital over differing periods of time.

(2) Mortgages backing privately issued pool securities and CMOs.

(3) Treasury securities accounted for less than 1 percent in 2005.

Source: Board of Governors of the Federal Reserve System, June 10, 2010.

($ billions, end of year)

(1) Includes Keoghs and other defined contribution plans, such as profit-sharing plans, without 401(k) features.

(2) Estimated.

Note: May not add to total due to rounding.

Source: Investment Company Institute.

(Percent, end of year)

Source: Federal Deposit Insurance Corporation.

(1) Includes savings banks and commercial banks; includes Keogh accounts.

(2) Includes Keogh accounts.

(3) Excludes variable annuities.

Source: Board of Governors of the Federal Reserve System, June 7, 2012.

Source: Board of Governors of the Federal Reserve System, June 10, 2010.

($ billions)

Source: Board of Governors of the Federal Reserve System.

($ billions, net premiums written)

Source: SNL Financial LC.

Source: SNL Financial LC.

(Percent change from prior year)

(1) Net premiums written, excluding state funds.

(2) Premiums and annuity considerations (fees for annuity contracts) for life/health insurance companies. Includes deposit-type funds beginning in 2001.

Source: SNL Financial LC.

($ billions)

(1) After reinsurance transactions, excluding state funds.

(2) Before reinsurance transactions; includes some state funds.

(3) Includes international and miscellaneous coverages.

(4) Premiums from certain insurers that write health insurance but file financial statements with state regulators on a property/casualty rather than life/health basis.

(5) Only includes nonproportional reinsurance, an arrangement in which a reinsurer makes payments to an insurer whose losses exceed a predetermined amount.

(6) Coverages protecting against legal liability resulting from negligence, carelessness, or failure to act.

Source: SNL Financial LC.

(£ millions)

(1) Values are in British pounds. 1998 breakdown is International Financial Services, London's estimate based on 1997 and 1999 data.

Source: Association of British Insurers; International Underwriting Association of London; Lloyd's; Carter and Falush: The London Insurance Market.

(1) Net premiums written, excluding state funds.

Source: SNL Financial LC.

(£ billions)

(1) Beginning of year.

Source: Lloyd's Members' Services Unit

Source: Swiss Re, sigma, No. 2/2010, update December 2010.

($ billions)

Source: Board of Governors of the Federal Reserve System, June 5, 2008.

($ billions)

(1) Includes individuals (including proprietors and partnerships), nonprofit institutions primarily serving individuals, life insurance carriers and miscellaneous entities.

Source: U.S. Department of Commerce, Bureau of Economic Analysis.

(1) Property/casualty: net premiums written, excluding state funds; life/health: premiums, annuity considerations (fees for annuity contracts) and deposit-type funds.

Source: SNL Financial LC.

($000)

(1) Indemnity costs per lost-time claim. 1991-2006: Based on data through 12/31/2006, developed to ultimate; based on the states where NCCI provides ratemaking services. Excludes the effects of deductible policies.

(2) Preliminary based on data valued as of 12/31/2007.

Source: NCCI Holdings, Inc.

(Percent of all U.S. households)

Source: Investment Company Institute, U.S. Bureau of the Census.

(Percent change from prior year)

(1) Net premiums written, excluding state funds.

(2) Premiums and annuity considerations (fees for annuity contracts) for life/health insurance companies.

Source: SNL Financial LC.

Source: Sallie Mae.

Source: © 2011 Munich Re, Geo Risks Research, NatCatSERVICE. As of April 2011.

(1) Long-term bonds with maturity dates over one year, as of December 31, 2011.

Source: SNL Financial LC.

†Overall agricultural crop losses were approximately $20 billion. $15-17 billion was recovered by the public-private multi-peril crop insurance program, making it the biggest loss in U.S. agricultural insurance history. In average years insured losses were around $9 billion.

Source: © 2013 Munich Re, NatCatSERVICE. As of January 2013.

(1) Cash and invested net admitted assets, as of December 31, 2011.

Source: SNL Financial LC.

(Number of events)

Source: © 2016 Munich Re, NatCatSERVICE. As of July 2016.

(1) Excluding state funds and residual markets.

Source: ISO, a Verisk Analytics company.

(Number of events, Annual totals 1980–2010 vs. first six months 2011)

Source: © 2011 Munich Re. NatCatSERVICE.

(1) Excludes state funds.

Source: ISO, a Verisk Analytics company.

(January – June Only, 1980 - 2012)

Source: 2012 Munich Re, NatCatSERVICE; The Property Claim Services (PCS) unit of ISO. As of July 2012.

(2011 $ billions)

(1) Estimated property losses adjusted for inflation through 2011 by ISO using the GDP implicit price deflator. Excludes catastrophes causing direct losses less than $25 million in 1997 dollars. Does not include flood damage covered by the federally administered National Flood Insurance Program.

(2) Excludes snow.

(3) Includes wildland fires.

(4) Includes losses from civil disorders, water damage, utility service disruptions, and any workers compensation catastrophes generating losses in excess of PCS's threshold after adjusting for inflation.

Source: The Property Claim Services (PCS) unit of ISO, a Verisk Analytics company.

(2015 $ billions)

Source: © 2016 Munich Re, NatCatSERVICE; Property Claim Services (PCS®)*, a Verisk Analytics® business. As of January 2016.

(Based on perils; US$ millions)

Source: © 2020 Munich Re, NatCatSERVICE; Property Claim Services (PCS®)*, a Verisk Analytics® business. As of June 2020.

(2019 $ billions)

Source: © 2020 Munich Re, Geo Risks Research, NatCatSERVICE. As of June 2020.

(2011 $ billions)

(1) Estimated property losses adjusted for inflation through 2011 by ISO using the GDP implicit price deflator. Excludes catastrophes causing direct losses less than $25 million in 1997 dollars. Does not include flood damage covered by the federally administered National Flood Insurance Program. Percentages do not sum to 100 due to rounding.

(2) Includes the other 47 states plus Washington, D.C., Puerto Rico, and the U.S. Virgin Islands.

Source: The Property Claim Services (PCS) unit of ISO, a Verisk Analytics company.

(1) Preliminary.

Source: LIMRA International.

(Based on first year collected premium)

(1) Includes brokers, stockbrokers and personal producing general agents.

(2) Includes career, multiline exclusive and home service agents.

(3) No producers are involved. Does not include direct marketing efforts involving agents.

(4) Includes financial institutions, worksite and other channels.

(5) Estimate.

Source: LIMRA’s U.S. Individual Life Insurance Sales Survey and LIMRA estimates.

($ billions, year-end)

Source: LIMRA International, The U.S. Individual Annuity Yearbook - 2009.

(1) Based on complaints submitted to the Internet Crime Complaint Center.

Source: Internet Crime Complaint Center.

Source: Insurance Research Council: Public Attitude Monitor, 2003.

($ billions)

Source: LIMRA International, The U.S. Individual Annuity Yearbook - 2009.

(1) Percentages are based on the total number of Consumer Sentinel Network complaints by calendar year. These figures exclude "Do Not Call" registry complaints.

Source: Federal Trade Commission.

(1) Excludes AIDS/HIV.

Source: JHA, Inc., 2004 Disability Rate Study & Risk Management Survey.

($ billions)

(1) Estimated.

Source: Kehrer-LIMRA.

Source: Federal Emergency Management Agency (FEMA).

($ millions)

Source: GC Securities and Guy Carpenter & Company, LLC.

Source: Federal Emergency Management Agency (FEMA).

(1) The symbols show the most affected regions. The map shows events with property losses and/or fatalities.

Source: © 2010 Münchener Rückversicherungs-Gesellschaft, Geo Risks Research, NatCatSERVICE – As of December 2010.

(1) Preliminary.

Source: LIMRA International.

(1) As reported by participating carriers. Duration from disability date, includes Elimination Period, for closed claims only.

(2) Excludes AIDS/HIV.

Source: JHA, Inc., 2004 Disability Rate Study & Risk Management Survey.![]()

(1) Excludes state funds.

Source: ISO.

(1) Average annual growth from 1970 through 1993; marks the beginning of the shift to managed care.

(2) Projected.

Source: Centers for Medicare and Medicaid Services, Office of the Actuary.

(1) Excluding state funds and residual markets.

Source: ISO.

($ billions)

(1) Single premium contracts bought by property/casualty insurers to distribute awards in personal injury or wrongful death lawsuits over a period of time, rather than as lump sums.

Source: LIMRA International.

($ millions)

(1) Based on total new premium.

Source: Kehrer-LIMRA.

($ billions)

(1) Excludes state funds.

(2) Net underwriting gain/loss plus net investment income.

Source: SNL Financial LC.

($ millions)

(1) Sales are gross premiums written.

Source: Organization for Economic Cooperation and Development.

(1) After reinsurance transactions, excluding state funds.

Source: SNL Financial LC.

(1) Based on states where the National Council on Compensation Insurance provides ratemaking services. Represents costs for injuries that resulted in time off from work. Data for 2011 are preliminary.

Source: U.S. Department of Commerce, Bureau of Labor Statistics; National Council on Compensation Insurance.

Source: U.S. Department of Labor, Bureau of Labor Statistics.

(1) Short-term and long-term disability.

Source: Eastbridge Consulting Group, Inc.

($ billions)

(1) Single premium contracts bought by property/casualty insurers to distribute awards in personal injury or wrongful death lawsuits over a period of time, rather than as lump sums.

Source: LIMRA International.

(1) Average annual growth from 1970 through 1993; marks the beginning of the shift to managed care.

(2) Projected.

Source: Centers for Medicare and Medicaid Services, Office of the Actuary, National Health Statistics Group.

(1) Includes co-payments, deductibles, and any amounts not covered by health insurance.

(2) Department of Veterans Affairs, Department of Defense and Children's Health Insurance Program.

Source: Centers for Medicare and Medicaid Services, Office of the Actuary, National Health Statistics Group.

Source: SNL Financial LC.

($ billions)

Source: The Property Claim Service (PCS) unit of ISO, a Verisk Analytics company. As of 7/23/13.

(Based on first year collected premium)

(1) Includes career, multiline exclusive and home service agents.

(2) Includes brokers and personal producing general agents.

(3) No producers are involved. Does not include direct marketing efforts involving agents.

(4) Includes stockbrokers, financial institutions, worksite and other channels.

(5) Estimate.

Source: LIMRA’s Market Share by Distribution Channel Survey, LIMRA estimates.

Source: The Property Claim Service (PCS) unit of ISO, a Verisk Analytics company. As of 7/23/13.

Source: U.S. Department of Commerce, Storm Prediction Center, National Weather Service.

Source: SNL Financial LC.

(1) Based on plaintiff and defendant verdicts rendered.

Source: Thomson Reuters.

(1) Cash and invested net admitted assets, as of December 31, 2009.

(2) Long-term bonds with maturity dates over one year.

Source: SNL Financial LC.

(1) Includes private insurance and FAIR plans.

Source: ISO, a Verisk Analytics company.

(Percent change from prior year)

(1) Percent change using seasonally adjusted data from prior year on an end-of-year basis.

Source: Board of Governors of the Federal Reserve System, June 7, 2012.

(1) Based on net premiums written, excludes state funds and other residual market carriers.

Source: ISO, a Verisk Analytics company.

($ billions, end of year)

Source: Board of Governors of the Federal Reserve System, June 7, 2012.

($ billions)

(1) After reinsurance transactions, excluding state funds.

(2) Before reinsurance transactions.

(3) Includes international and miscellaneous coverages.

(4) Premiums from certain insurers that write health insurance but file financial statements with state regulators on a property/casualty rather than life/health basis.

(5) Only includes nonproportional reinsurance, an arrangement in which a reinsurer makes payments to an insurer whose losses exceed a predetermined amount.

(6) Coverages protecting against legal liability resulting from negligence, carelessness, or failure to act.

Source: SNL Financial LC.

($ billions)

Source: 2009 to 2011 premiums from Business Insurance, October 8, 2012; earlier premiums from other issues.

($ billions, end of year)

(1) Preliminary data. Excludes defined benefit plans.

Source: Investment Company Institute. 2021. 2021 Investment Company Fact Book: A Review of Trends and Activities in the U.S. Investment Company Industry. Washington, D.C. Investment Company Institute. www.icifactbook.org.

(1) Short-term and long-term disability.

Source: Eastbridge Consulting Group, Inc.

Source: Board of Governors of the Federal Reserve System, June 7, 2012.

($ billions)

Source: Board of Governors of the Federal Reserve System.

Source: © 2013 Munich Re, Geo Risks Research, NatCatSERVICE. As of January 2013.

(1) Mortgages backing privately issued pool securities and collateralized mortgage obligations (CMOs).

(2) Securities of federal mortgage pools backing privately issued CMOs. In CMOs, mortgage principal and interest payments are separated into different payment streams to create bonds that repay capital over differing periods of time.

Source: Board of Governors of the Federal Reserve System, June 7, 2012.

(2009 $ billions)

(1) Catastrophes are all events causing direct insured losses to property of $25 million or more in 2009 dollars. Adjusted for inflation by ISO.

(2) Excludes snow.

(3) Does not include flood damage covered by the federally administered National Flood Insurance Program.

(4) Includes wildland fires.

(5) Includes civil disorders, water damage, utility service disruptions and non-property losses such as those covered by workers compensation.

Source: ISO's Property Claim Services (PCS) unit.

(Number of events)

Source: © 2013 Munich Re, Geo Risks Research, NatCatSERVICE. As of January 2013.

Source: Investment Company Institute.

(1) Includes Fannie Mae and Freddie Mac. GSEs are government-sponsored enterprises.

Source: Federal Housing Finance Agency.

(Overall and insured losses)

Source: © 2013 Munich Re, Geo Risks Research, NatCatSERVICE. As of January 2013.

($ millions)

* Data based on information from PCS.

Source: © 2016 Munich Re, Geo Risks Research, NatCatSERVICE. As of January 2016.

(Market value, end of year)

(1) Excludes variable annuities.

(2) Includes Keogh accounts.

(3) Includes savings banks, commercial banks and Keogh accounts.

Source: Board of Governors of the Federal Reserve System, June 10, 2021.

(1) HECMs are federally insured reverse mortgage products.

(2) Through July 2010; fiscal year ends September 30.

Source: National Reverse Mortgage Lenders Association.

Source: © 2013 Munich Re, NatCatSERVICE. As of July 2013.

Source: U.S. Department of Commerce, Bureau of Economic Analysis.

(Percent)

Source: U.S. Department of Commerce, Census Bureau; Housing Vacancy Survey.

(Overall and insured losses)

Source: © 2013 Munich Re, NatCatSERVICE; The Property Claim Services (PCS) unit of ISO. As of January 2013.

Source: U.S. Department of Commerce, Bureau of Economic Analysis.

(1) Estimated.

Source: American Bankers Association.

(Number of events)

Source: © 2013 Munich Re, NatCatSERVICE. As of January 2013.

($ billions)

Source: Board of Governors of the Federal Reserve System.

(1) As of July 31, 2018.

Source: Federal Emergency Management Agency (FEMA).

(Annual totals 1980–2012)

Source: 2013 Munich Re, NatCatSERVICE; The Property Claim Services (PCS) unit of ISO. As of January 2013.

(000)

Source: U.S. Department of Labor, Bureau of Labor Statistics.

(1) Average annual growth from 1970 through 1993; marks the beginning of the shift to managed care.

(2) Projected.

Source: Centers for Medicare and Medicaid Services, Office of the Actuary.

Source: © 2013 Munich Re, NatCatSERVICE; NOAA. As of January 2013.

(1) Market value, end of year; excludes open-end mutual fund shares.

(2) Holdings of U.S. issues by foreign residents.

Source: Board of Governors of the Federal Reserve System, June 7, 2012.

($ billions)

(1) Excludes state funds.

(2) Net underwriting gain/loss plus net investment income.

Source: SNL Financial LC.

Source: 2013 Munich Re, NatCatSERVICE; The Property Claim Services (PCS) unit of ISO; National Flood Insurance Plan. As of January 2013.

Source: U.S. Individual Annuities, GLIMPSE Quarterly Reports, LIMRA Secure Retirement Institute.

($ billions)

(1) Projected.

Source: Celent.

($ billions, 2013 dollars)

(1) $1 billion economic loss and/or 50 fatalities, as of January 7, 2014. Losses based on property losses including, if applicable, agricultural, offshore, marine, aviation and National Flood Insurance Program losses and may differ from data shown elsewhere.

Source: © 2014 Munich Re. NatCatSERVICE.

($ billions)

(1) Single premium contracts bought by property/casualty insurers to distribute awards in personal injury or wrongful death lawsuits over a period of time, rather than as lump sums. Classified as a fixed annuity.

Source: LIMRA International.

(1) After reinsurance transactions, excluding state funds.

Source: SNL Financial LC.

Note: U.S. insured losses for Hurricane Irene includes National Flood Insurance Program (NFIP) claims. The U.S. insured loss for Tropical storm Lee does not include NFIP losses.

Source: © 2011 Münchener Rückversicherungs-Gesellschaft, Geo Risks Research, NatCatSERVICE. As of November 2011.

($ millions)

(1) Based on total new premiums.

Source: Bank Insurance and Securities Research Associates (BISRA).

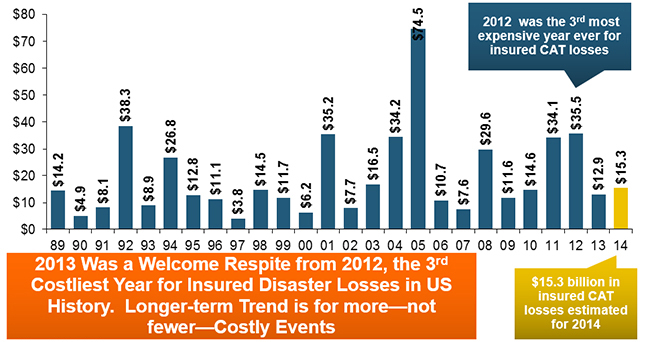

($ Billions) (Stated in 2006 Dollars)

Source: National Weather Service.

(1) Based on a survey of insurance departments by the NAIC. May vary somewhat from data based on annual statement filings.

(2) Blue Cross/Blue Shield, HMOs and hospital, medical and dental indemnity.

Source: National Association of Insurance Commissioners (NAIC). Reprinted with permission. Further reprint or redistribution strictly prohibited without written permission of NAIC.

(1) Reported to local fire departments.

Source: National Fire Protection Association.

Source: 1900-1950: U.S. Department of Commerce, Census Bureau, Census of Housing. 1960-present: Census Bureau, Housing Vacancy Survey.

Source: SNL Financial LC.

Source: © 2016 Munich Re, Geo Risks Research, NatCatSERVICE. As of January 2016.

(1) Data prior to 2009 not strictly comparable to earlier data.

Source: National Association of State Treasurers.

($ billions)

Source: Organization for Economic Cooperation and Development.

($ millions)

*U.S. losses from Property Claim Services.

Source: © 2016 Munich Re, Geo Risks Research, NatCatSERVICE. As of January 2016.

(1) Includes finance company subsidiaries of bank holding companies but not of retailers and banks. Includes owned receivables (carried on the balance sheet of the institution) and managed receivables (outstanding balances of pools upon which securities have been issued; these balances are no longer carried on the balance sheets of the loan originator).

Source: Board of Governors of the Federal Reserve System.

(US$ billions)

Source: Organization for Economic Cooperation and Development.

Source: © 2016 Munich Re, Geo Risks Research, NatCatSERVICE. As of January 2016.

(US$ billions)

(1) Before reinsurance transactions.

(2) Includes accident and health insurance.

Source: Swiss Re Institute, sigma, 2/2025.

(1) Includes co-payments, deductibles, and any amounts not covered by health insurance.

(2) Department of Veterans Affairs, Department of Defense and Children's Health Insurance Program.

Source: Centers for Medicare and Medicaid Services, Office of the Actuary, National Health Statistics Group.

($ billions, net premiums written)

Source: SNL Financial LC.

Source: National Fire Protection Association.

Source: SNL Financial LC.

($ billions)

Source: GC Securities, a division of MMC Securities Corp., a U.S. registered broker-dealer, member FINRA/SIPC and Guy Carpenter.

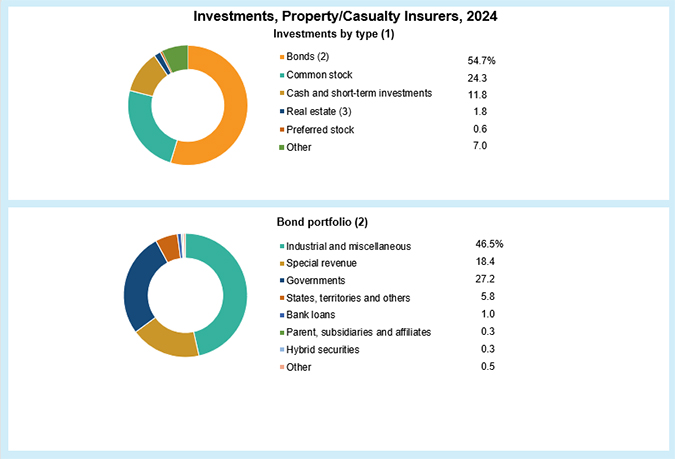

(1) Cash and invested net admitted assets, as of December 31, 2024.

(2) Bonds represents 54.7% of total investments.

(3) Includes mortgage loans on real estate.

Source: NAIC data, sourced from S&P Global Market Intelligence, Insurance Information Institute.

($ billions)

Source: GC Securities, a division of MMC Securities Corp., a U.S. registered broker-dealer, member FINRA/SIPC and Guy Carpenter.

Source: © 2013 Munich Re. NatCatSERVICE; National Interagency Fire Center. As of January 2013.

(Percent)

(1) Loss experience in the past 5 years.

Source: 2008 Limits of Liability Report, © Marsh Inc. 2008.

(Five costliest events ordered by overall losses)

Source: © 2016 Munich Re, NatCatSERVICE; Property Claim Services (PCS®)*, a Verisk Analytics® business. As of February 2016.

(Average limits purchased, $ millions)

(1) Loss experience in the past 5 years.

Source: 2008 Limits of Liability Report, © Marsh Inc, 2008.

($ billions)

(1) Includes individuals (including proprietors and partnerships), nonprofit institutions primarily serving individuals, life insurance carriers and miscellaneous entities.

Source: U.S. Department of Commerce, Bureau of Economic Analysis.

(1) Includes deaths resulting from conflagration, regardless of nature of injury.

(2) Inhalation and ingestion of food or other object that obstructs breathing.

Source: National Safety Council.

Source: Jury Verdict Research.

(1) Percentages are based on the total number of Consumer Sentinel Network reports by calendar year. These figures exclude "Do Not Call" registry complaints.

Source: Federal Trade Commission, Consumer Sentinel Network.

($000)

(1) Represents the midpoint jury award. Half of awards are above the median and half are below.

Source: Reprinted with permission from Current Award Trends in Personal Injury. Copyright 2010 by LRP Publications, 747 Dresher Road, P.O. Box 980, Horsham, PA 19044-0980. All rights reserved.

($ trillions, end of year)

(1) Data for 2003, 2009, 2010 and 2011 are estimates.

Source: Investment Company Institute.

Source: Reprinted with permission of Thomson Reuters, Current Award Trends in Personal Injury, 54th edition.

Source: U.S. Department of Labor, Bureau of Labor Statistics.

(US$ billions)

(1) Property/casualty: net premiums written after reinsurance transactions, excludes state funds; life/annuity: premiums, annuity considerations (fees for annuity contracts) and deposit-type funds. Both sectors include accident and health insurance.

Source: NAIC data, sourced from S&P Global Market Intelligence: Insurance Expense Exhibits, Summary of Operations; Insurance Information Institute.

($ billions)

Source: 2007 to 2009 premiums from Business Insurance, October 11, 2010; earlier premiums from other issues.

($ billions)

(1) After reinsurance transactions, excludes state funds.

(2) Before reinsurance transactions, includes some state funds.

(3) Includes miscellaneous coverages.

(4) Includes federally sponsored multiple peril crop and private market crop-hail.

(5) Premiums from certain insurers that write health insurance but file financial statements with state regulators on a property/casualty rather than life/health basis.

(6) Only includes nonproportional reinsurance, an arrangement in which a reinsurer makes payments to an insurer whose losses exceed a predetermined amount.

(7) Coverages protecting against legal liability resulting from negligence, carelessness or failure to act.

Source: NAIC data, sourced from S&P Global Market Intelligence, Insurance Information Institute.

Source: © 2011 Munich Re, Geo Risks Research, NatCatSERVICE. As of July 2011.

($ billions)

Source: NAIC data, sourced from S&P Global Market Intelligence, Insurance Information Institute.

Source: Pew Internet and American Life Project.

(1) Based on net premiums written, excluding state funds.

Source: ISO.

(End of year)

Source: Federal Deposit Insurance Corporation (FDIC).

Source: Securities Industry and Financial Markets Association.

($ billions)

(1) Represents homeowners' cash withdrawals from home mortgage refinance transactions. Includes prime conventional loans only and is net of retirement of outstanding second mortgages.

(2) Estimated.

Source: Freddie Mac.

(000)

Source: Securities Industry and Financial Markets Association.

Source: Securities Industry and Financial Markets Association.

(Percent)

(1) New York Stock Exchange reporting firms doing public business.

Source: Securities Industry and Financial Markets Association.

($ billions)

(1) New York Stock Exchange reporting firms doing public business.

Source: Securities Industry and Financial Markets Association.

($ billions)

Source: Securities Industry and Financial Markets Association.

Source: McKinsey IICF survey, Center for Encouraging Corporate Philanthropy, Giving by Numbers 2010, McKinsey analysis.

Source: SNL Financial LC.

(End of year)

Source: Investment Company Institute.

($ billions)

(1) Estimated.

Source: Celent.

(1) HECMs are federally insured reverse mortgage products.

(2) Through April 2012; fiscal year ends September 30.

Source: National Reverse Mortgage Lenders Association.

Source: Investment Company Institute.

($B, Adjusted to 2008 Price Level)

(1) Estimated September 11 industry loss at 2001 price level is $32.5 billion.

Source: Insurance Information Institute.

(Overall and insured losses, 2015 $billions)

Source: © 2016 Munich Re, NatCatSERVICE; Property Claim Services (PCS®)*, a Verisk Analytics® business. As of July 2016.

(Percent)

(1) New York Stock Exchange reporting firms doing public business in the United States.

Source: NYSE Euronext; Securities Industry and Financial Markets Association.

(1) Based on selected components of underwriting as a percent of net premiums earned, rebased to 100.0 percent.

(2) Taxes, licenses, fees, acquisitions, field supervision, collection and general expenses.

Source: SNL Financial LC.

($ billions)

(1) New York Stock Exchange reporting firms doing public business in the United States.

Source: NYSE Euronext; Securities Industry and Financial Markets Association.

(1) Based on selected components of underwriting as a percent of net premiums earned, rebased to 100.0 percent.

(2) Taxes, licenses, fees, acquisitions, field supervision, collection and general expenses.

Source: SNL Financial LC.

($ billions)

(1) As of January.

Source: Hennessee Group, LLC.

Source: © 2014 Munich Re, Geo Risks Research, NatCatSERVICE. As of January 2014.

(1) The states of Alabama, Florida, and Minnesota did not provide monthly breakdowns for offense and are not included in the monthly variations.

Source: U.S. Department of Justice, Federal Bureau of Investigation.

(1) Percent of drivers using hand-held cellphones.

Source: U.S. Department of Transportation, National Highway Traffic Safety Administration.

(1) Based on participants in the survey that reported one or more claims over the five-year period.

Source: JLT Specialty 2015 U.S. Directors and Officers Liability Survey.

*Only includes tenants or renters insurance on the contents of a residence.

**Bureau of Labor Statistics’ Producer Price Index (preliminary).

***Median sales price. Data from the National Association of Realtors.

(1) Based on participants in the survey that reported one or more claims over the 10-year period.

Source: 2011 Directors and Officers Liability Survey, Towers Watson.

Source: © 2011 Munich Re, Geo Risks Research, NatCatSERVICE. As of October 2011.

(1) Based on participants in the survey that reported one or more claims over the four-year period.

Source: JLT Specialty 2015 U.S. Directors and Officers Liability Survey.

(Annual totals 1980 – 2011)

Source: © 2012 Munich Re. NatCatSERVICE.

(1) Estimated insured losses are based on property losses including, if applicable, agricultural, offshore, marine, aviation and National Flood Insurance Program losses and may differ from data shown elsewhere. As of July 6, 2011.

(2) Severe thunderstorm includes tornadoes.

(3) Tropical cyclone includes hurricanes.

Source: © 2011 Munich Re. NatCatSERVICE.

(Number of events, January-June only)

Source: © 2011 Munich Re. NatCatSERVICE.

(January – June only, 1980-2011)

Source: © 2011 Munich Re. NatCatSERVICE.

(2016 $ billions)

(1) Adjusted for inflation through 2016 by ISO using the GDP implicit price deflator. Excludes catastrophes causing direct losses less than $25 million in 1997 dollars. Excludes flood damage covered by the federally administered National Flood Insurance Program.

(2) Includes other wind, hail, and/or flood losses associated with catastrophes involving tornadoes.

(3) Includes wildland fires.

(4) Includes losses from civil disorders, water damage, utility service disruptions, and any workers compensation catastrophes generating losses in excess of PCS's threshold after adjusting for inflation.

Source: The Property Claim Services® (PCS®) unit of ISO®, a Verisk Analytics® company.

(Annual totals 1980–2010 vs. first half 2011)

Source: © 2011 Munich Re. NatCatSERVICE.

Source: Board of Governors of the Federal Reserve System, June 10, 2021.

Source: © 2014 Munich Re, NatCatSERVICE; Property Claim Services (PCS®)*, a Verisk Analytics® business; National Flood Insurance Plan. As of January 2014.

(1) Includes co-payments, deductibles, and any amounts not covered by health insurance.

(2) Department of Veterans Affairs, Department of Defense and Children's Health Insurance Program.

Source: Centers for Medicare and Medicaid Services, Office of the Actuary, National Health Statistics Group.

Source: SNL Financial LC.

(1) Includes other non-occupants.

Source: U.S. Department of Transportation, National Highway Traffic Safety Administration.

(000)

(1) Deferred status refers to individuals eligible for future payments.

(2) Payees are retired participants or their beneficiaries receiving payments.

Source: Pension Benefit Guaranty Corporation.

Source: U.S. Department of Commerce, Bureau of Economic Analysis.

($ billions)

(1) Excludes premiums of Lloyd’s of London syndicates.

Source: Business Insurance (www.businessinsurance.com), September 2017.

Source: U.S. Department of Commerce, Bureau of Economic Analysis.

Note: Percentages do not add up to 100 percent due to rounding.

(1) Excludes insurance.

Source: U.S. Department of Labor, Bureau of Labor Statistics.

Source: National Fire Protection Association.

($ billions)

Source: NAIC data, sourced from S&P Global Market Intelligence, Insurance Information Institute.

Source: U.S. Department of Commerce, National Oceanic and Atmospheric Administration, National Weather Service and National Lightning Safety Council.

($ billions)

Source: NAIC data, sourced from S&P Global Market Intelligence, Insurance Information Institute.

Source: NAIC data, sourced from S&P Global Market Intelligence, Insurance Information Institute.

(1) Reported to local fire departments.

Source: National Fire Protection Association.

(000)

Source: U.S. Department of Commerce, Census Bureau.

Source: U.S. Department of Commerce, Storm Prediction Center, National Weather Service.

(1) Percent of all drivers using handheld cellphones.

Source: U.S. Department of Transportation, National Highway Traffic Safety Administration.

($ millions)

(1) Based on total new premium.

Source: Kehrer-LIMRA.

($ U.S. dollars)

($ billions, excludes state funds)

(1) Includes deposit type funds beginning in 2001.

Source: National Association of Insurance Commissioners (NAIC) Annual Statement Database, via Highline Data, LLC. Copyrighted information. No portion of this work may be copied or redistributed without the express written permission of Highline Data, LLC.

($ millions)

Source: GC Securities and Guy Carpenter & Company, LLC.

(Premiums and investments)

($ millions)

Source: GC Securities and Guy Carpenter & Company, LLC.

(Premiums and investments)

(1) Based on participants in the survey that reported one or more claims over the 10-year period.

Source: 2010 Directors and Officers Liability Survey, Towers Watson.

($ 2024 billions)

(1) Adjusted to 2024 dollars by the Insurance Information Institute using the U.S. Department of Labor BLS Calculator.

(2) Loss total does not include March 2010 New York City settlement of up to $657.5 million to compensate approximately 10,000 Ground Zero workers or any subsequent settlements.

Source: Insurance Information Institute.

(1) Based on participants in the survey that reported one or more claims over the 10-year period.

Source: 2010 Directors and Officers Liability Survey, Towers Watson.

(1) Based on data in the National Association of Independent Insurers, 2002 Survey on the Use of Credit Information in Personal Lines Insurance; NAII is one of the predecessor organizations to the Property Casualty Insurers of America.

Source: Property Casualty Insurers Association of America.

Source: Jury Verdict Research.

($ billions)

Source: Board of Governors of the Federal Reserve System, June 7, 2012.

(1) Based on participants in the survey that reported one or more claims over the 10-year period.

Source: 2010 Directors and Officers Liability Survey, Towers Watson.

($000)

(1) 1999-2007: Based on data through 12/31/2007, developed to ultimate; based on the states where NCCI provides ratemaking services, including state funds. Excludes high deductible policies.

(2) Preliminary based on data valued as of 12/31/2008.

Source: NCCI Holdings, Inc.

(000)

Source: U.S. Department of Labor, Bureau of Labor Statistics.

(1) Percentages are dollar weighted averages.

Source: Investment Company Institute.

(000)

(1) Deferred status refers to individuals eligible for future payments.

(2) Payees are retired participants or their beneficiaries receiving payments.

Source: Pension Benefit Guaranty Corporation.

(1) Does not add to total due to rounding.

Source: Investment Company Institute.

(1) State Children's Health Insurance Program.

(2) Includes programs such as workers compensation, public health activity, Department of Defense, Department of Veterans Affairs, Indian Health Service, state and local hospital subsidies and school health.

(3) Includes industrial in-plant, privately funded construction and nonpatient revenues, including philanthropy.

Source: Centers for Medicare and Medicaid Services, Office of the Actuary.

Source: Investment Company Institute.

(Percent of all U.S. households)

Source: Investment Company Institute, U.S. Bureau of the Census.

($ trillions, year-end)

Source: Investment Company Institute.

($ trillions, year-end)

Source: Investment Company Institute.

(1) Average annual growth from 1970 through 1993; 1993 marked the beginning of the shift to managed care.

(2) Projected.

Source: Centers for Medicare and Medicaid Services, Office of the Actuary.

($ trillions, end of year)

(1) Data for 2003, 2005, 2008, 2009 and 2010 are estimates. Data for 2006 and 2007 are preliminary.

Source: Investment Company Institute.

(000)

Source: U.S. Department of Labor, Bureau of Labor Statistics.

(1) Percentages are dollar-weighted averages.

Source: Investment Company Institute.

(000)

Source: U.S. Department of Labor, Bureau of Labor Statistics.

($ billions, end of year)

(1) Includes Keoghs and other defined contribution plans, such as profit-sharing plans, without 401(k) features.

(2) Estimated.

Source: Investment Company Institute.

Source: © 2020 Munich Re, Geo Risks Research, NatCatSERVICE. As of January 2020.

($ billions)

(1) Single premium contracts bought by property/casualty insurers to distribute awards in personal injury or wrongful death lawsuits over a period of time, rather than as lump sums.

Source: LIMRA International.

Source: U.S. Department of Commerce, Storm Prediction Center, National Weather Service.

(1) Percentages are based on the total number of Consumer Sentinel Network complaints by calendar year. These figures exclude "Do Not Call" registry complaints.

Source: Federal Trade Commission.

(1) Excludes state-run insurers.

(2) Insurance Information Institute Estimates/Forecasts.

Source: NAIC, Insurance Information Institute estimates 2008-2010 based on CPI data.

(Percent of all U.S. households)

Source: Investment Company Institute, U.S. Bureau of the Census.

(Deadliest and costliest events)

Source: © Munich Re, Geo Risks Research, NatCatSERVICE. As of August 2014.

($ trillions, end of year)

(1) Data for 2003, 2005, 2006, 2007 and 2008 are estimates.

Source: Investment Company Institute.

($ billions, end of year)

(1) Preliminary data. Does not include defined benefit plans.

Source: Investment Company Institute.

($ trillions, year-end)

(1) Estimated.

Source: Investment Company Institute. 2021. 2021 Investment Company Fact Book: A Review of Trends and Activities in the U.S. Investment Company Industry. Washington, D.C. Investment Company Institute. www.icifactbook.org.

($000)

(1) Represents the midpoint jury award. Half of awards are above the median and half are below.

Source: Reprinted with permission from Current Award Trends in Personal Injury. Copyright 2009 by LRP Publications, 747 Dresher Road, P.O. Box 980, Horsham, PA 19044-0980. All rights reserved.

(1) Percentages are based on the total number of Consumer Sentinel Network complaints by calendar year. These figures exclude "Do Not Call" registry complaints.

Source: Federal Trade Commission.

($ millions)

Source: Guy Carpenter: GC Securities.

CATASTROPHE BONDS, RISK CAPITAL OUTSTANDING, 2004-2008

($ millions)

Source: Guy Carpenter: GC Securities.

(1) Data prior to 2009 not strictly comparable to earlier data.

Source: National Association of State Treasurers.

Source: LIMRA International.

Source: Federal Deposit Insurance Corporation.

(Based on dollar value)

(1) Based on a survey by claims aggregator, Enservio, of the replacement cost value of homeowners insurance property content claims. Includes items that are damaged, lost or stolen.

Source: Enservio.

(1) Securities of federal mortgage pools backing privately issued collateralized mortgage obligations (CMOs). In CMOs, mortgage principal and interest payments are separated into different payment streams to create bonds that repay capital over differing periods of time.

(2) Mortgages backing privately issued pool securities and CMOs.

(3) Treasury securities accounted for less than 1 percent in 2004.

Source: Board of Governors of the Federal Reserve System, June 11, 2009.

(Percent)

Source: Federal Deposit Insurance Corporation.

($ billions)

Source: Board of Governors of the Federal Reserve System.

(1) HECMs are federally insured reverse mortgage products.

(2) Through July 2010; fiscal year ends September 30.

Source: National Reverse Mortgage Lenders Association.

Source: Board of Governors of the Federal Reserve System, June 11, 2009.

(1) Estimated.

Source: American Bankers Association.

(1) Market value, end of year; excludes open-end mutual fund shares.

(2) Holdings of U.S. issues by foreign residents.

Source: Board of Governors of the Federal Reserve System, June 11, 2009.

(Weighted average, 2005-2009)

(1) For homeowners multiple peril policies. Excludes tenants and condominium owners policies. Accident year incurred losses, excluding loss adjustment expenses, i.e., indemnity costs per accident year incurred claims.

(2) Includes coverage for unauthorized use of various cards, forgery, counterfeit money and losses not otherwise classified.

(3) Includes vandalism and malicious mischief.

Source: ISO, a Verisk Analytics company.

(Percent change from prior year)

Source: Board of Governors of the Federal Reserve System, June 11, 2009.

(Weighted average, 2005-2009)

(1) Claims per 100 house years (policies). For homeowners multiple peril policies. Excludes tenants and condominium owners policies.

(2) Includes vandalism and malicious mischief.

(3) Includes coverage for unauthorized use of various cards, forgery, counterfeit money and losses not otherwise classified.

Source: ISO, a Verisk Analytics company.

($ billions, end of year)

Source: Board of Governors of the Federal Reserve System, June 11, 2009.

(1) Average annual growth from 1970 through 1993; marks the beginning of the shift to managed care.

(2) Projected.

Source: Centers for Medicare and Medicaid Services, Office of the Actuary.

Source: Board of Governors of the Federal Reserve System, June 11, 2009.

(1) Market value, end of year; excludes open-end mutual fund shares.

(2) Holdings of U.S. issues by foreign residents.

Source: Board of Governors of the Federal Reserve System, June 9, 2011.

(1) Does not add to total due to rounding.

Source: Investment Company Institute.

(1) Percent change from prior year on an end-of-year basis.

Source: Board of Governors of the Federal Reserve System, June 9, 2011.

(1) Percentages are dollar weighted averages.

Source: Investment Company Institute.

Source: Board of Governors of the Federal Reserve System, June 9, 2011.

($ billions)

(1) Single premium contracts bought by P/C insurers to distribute awards in personal injury or wrongful death lawsuits over a period of time, rather than as lump sums.

Source: LIMRA International.

(End of year)

(1) Includes savings banks and commercial banks.

(2) Puerto Rico, the U.S. Virgin Islands, American Samoa, Guam and other U.S.-affiliated insular areas.

Source: Board of Governors of the Federal Reserve System, June 7, 2012.

($ billions)

(1) Preliminary data.

Source: Investment Company Institute.

Source: Securities Industry and Financial Markets Association.

Source: Federal Deposit Insurance Corporation.

(1) Mortgages backing privately issued pool securities and CMOs.

(2) Securities of federal mortgage pools backing privately issued collateralized mortgage obligations (CMOs). In CMOs, mortgage principal and interest payments are separated into different payment streams to create bonds that repay capital over differing periods of time.

Source: Board of Governors of the Federal Reserve System, June 9, 2011.

Source: Investment Company Institute.

($ billions)

Source: Board of Governors of the Federal Reserve System.

Source: Board of Governors of the Federal Reserve System, June 9, 2011.

Source: © Munich Re, Geo Risks Research, NatCatSERVICE. As of March 29, 2010.

($ billions)

(1) Includes individuals (including proprietors and partnerships), nonprofit institutions primarily serving individuals, life insurance carriers and miscellaneous entities.

Source: U.S. Department of Commerce, Bureau of Economic Analysis.

(1) Excludes state funds.

Source: ISO.

(1) Based on complaints submitted to the Internet Crime Complaint Center.

Source: Internet Crime Complaint Center.

(1) Catastrophes are all events causing direct insured losses to property of $25 million or more in 2008 dollars. Adjusted for inflation by ISO.

(2) Excludes snow.

(3) Does not include flood damage covered by the federally administered National Flood Insurance Program.

(4) Includes civil disorders, water damage, fires other than wildlfires and utility service disruptions.

Source: ISO's Property Claim Services unit (PCS).

Source: 1900-1950: U.S. Census Bureau, Census of Housing. 1960-present: U.S. Census Bureau, Housing Vacancy Survey.

(1) Excluding state funds and residual markets.

Source: ISO.

Source: Sallie Mae.

(1) Gross direct premiums. Total premiums for 2008 were $1,626 billion.

(2) Blue Cross/Blue Shield, HMOs and hospital, medical and dental indemnity.

Source: National Association of Insurance Commissioners. Reprinted with permission. Further reprint or redistribution strictly prohibited without written permission of NAIC.

Source: © 2012 Munich Re, Geo Risks Research, NatCatSERVICE. As of January 2012.

Source: U.S. Department of Commerce, Bureau of Economic Analysis.

(1980 – 2011)

Source: © 2012 Münchener Rückversicherungs-Gesellschaft, Geo Risks Research, NatCatSERVICE. As of January 2012.

Source: U.S. Department of Commerce, Bureau of Economic Analysis.

(Overview and comparison with previous years)

Source: © 2012 Munich Re, Geo Risks Research, NatCatSERVICE. As of July 2012.

($ billions)

(1) Represents homeowners' cash withdrawals from home mortgage refinance transactions. Includes prime conventional loans only and is net of retirement of outstanding second mortgages.

(2) Estimated.

Source: Freddie Mac.

(Number of relevant events by peril)

Source: © 2019 Munich Re, Geo Risks Research, NatCatSERVICE. As of March 2019.

($ billions)

(1) Includes individuals; nonprofit institutions primarily serving individuals; private noninsured welfare funds; and private trust funds.

Source: U.S. Department of Commerce, Bureau of Economic Analysis.

Source: © 2019 Munich Re, Geo Risks Research, NatCatSERVICE. As of March 2019.

($ billions)

Source: LIMRA International, The 2008 Individual Annuity Market - Sales and Assets Report.

(The five costliest natural catastrophes for the insurance industry)

Source: © 2013 Munich Re, Geo Risks Research, NatCatSERVICE. As of January 2013.

Source: © 2021 Munich Re, Geo Risks Research, NatCatSERVICE. As of January 2021.

(Percent, end of year)

Source: Federal Deposit Insurance Corporation.

(1980 – 2011)

Source: © 2012 Münchener Rückversicherungs-Gesellschaft, Geo Risks Research, NatCatSERVICE. As of January 2012.

($ billions)

(1) Estimated.

Source: Kehrer-LIMRA.

Source: © 2012 Munich Re. NatCatSERVICE.

Source: Swiss Re, sigma, No. 3/2009.

(Number of events, Annual totals 1980–2010 vs. first six months 2011)

Source: © 2012 Munich Re. NatCatSERVICE.

(Percent change from prior year)

(1) Net premiums written, excluding state funds.

(2) Premiums and annuity considerations for life/health insurance companies. Includes deposit-type funds beginning in 2001.

Source: National Association of Insurance Commissioners (NAIC) Annual Statement Database, via Highline Data, LLC. Copyrighted information. No portion of this work may be copied or redistributed without the express written permission of Highline Data, LLC.

Source: © 2014 Munich Re, NatCatSERVICE; NOAA. As of January 2014.

($ billions)

Source: National Association of Insurance Commissioners (NAIC) Annual Statement Database, via Highline Data, LLC. Copyrighted information. No portion of this work may be copied or redistributed without the express written permission of Highline Data, LLC.

Source: © 2012 Munich Re, The Property Claim Services (PCS) unit of ISO, NatCatSERVICE, National Flood Insurance Plan.

(1) Excluding state funds.

Source: National Association of Insurance Commissioners (NAIC) Annual Statement Database, via Highline Data, LLC. Copyrighted information. No portion of this work may be copied or redistributed without the express written permission of Highline Data, LLC.

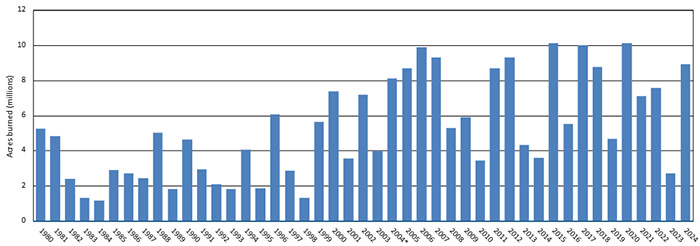

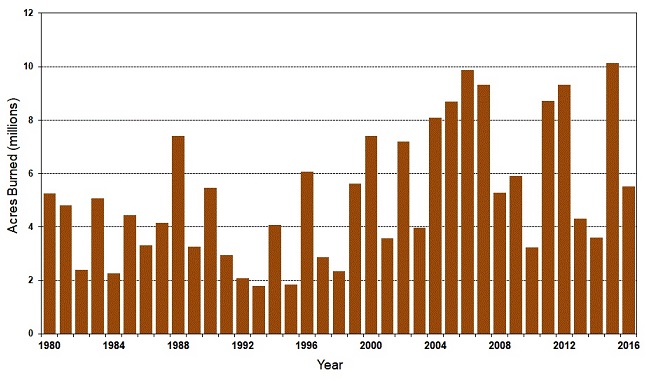

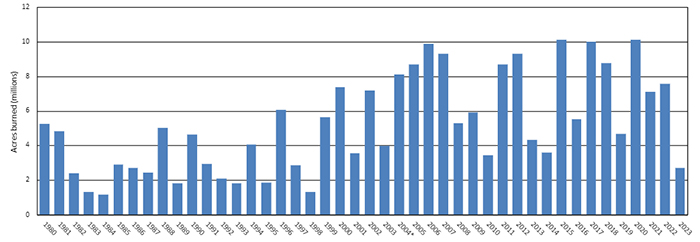

*2004 fires and acres do not include state lands for North Carolina.

Source: National Interagency Fire Center.

Source: SNL Financial LC.

($ billions, 2014 dollars)

(1) Does not include National Flood Insurance Program losses.

*Through 6/30/15 in 2015 dollars.

Note: 2001 figure includes $20.3B for 9/11 losses reported through 12/31/01 ($25.9B 2011 dollars). Includes only business and personal property claims, business interruption and auto claims. Non-prop/BI losses = $12.2B ($15.6B in 2011 dollars.)

Source: Property Claim Services (PCS®), a Verisk Analytics® business; AonBenfield; Insurance Information Institute. As of June 2015.

(1) Based on net premiums written, excluding state funds.

Source: ISO.

(1) Property/casualty: net premiums written, excluding state funds; Life/health: premiums, annuity considerations (fees for annuity contracts) and deposit-type funds.

Source: SNL Financial LC.

(1) Short-term and long-term disability.

Source: Eastbridge Consultants.

(Based on first year collected premium)

(1) Includes career, multiline exclusive and home service agents.

(2) Includes brokers and personal producing general agents.

(3) No producers are involved. Does not include direct marketing efforts involving agents.

(4) Includes stockbrokers, financial institutions, worksite and other channels.

(5) Estimate.

Source: LIMRA’s Market Share by Distribution Channel Survey, LIMRA estimates.

(Percent change from prior year)

(1) Net premiums written, excluding state funds.

(2) Premiums and annuity considerations (fees for annuity contracts) for life/health insurance companies. Includes deposit-type funds beginning in 2001.

Source: SNL Financial LC.

($ billions)

(1) After reinsurance transactions, excluding state funds.

(2) Before reinsurance transactions, excluding state funds. May not match total premiums shown elsewhere in this book because of the use of different exhibits from Highline Data LLC.

(3) Includes international and miscellaneous coverages.

(4) Premiums from certain insurers that write health insurance but file financial statements with state regulators on a property/casualty rather than life/health basis.

(5) Only includes nonproportional reinsurance, an arrangement in which a reinsurer makes payments to an insurer whose losses exceed a predetermined amount.

(6) Coverages protecting against legal liability resulting from negligence, carelessness, or failure to act.

Source: National Association of Insurance Commissioners (NAIC) Annual Statement Database, via Highline Data, LLC. Copyrighted information. No portion of this work may be copied or redistributed without the express written permission of Highline Data, LLC.

($ billions)

(1) After reinsurance transactions, excluding state funds.

(2) Before reinsurance transactions; includes some state funds.

(3) Includes international and miscellaneous coverages.

(4) Premiums from certain insurers that write health insurance but file financial statements with state regulators on a property/casualty rather than life/health basis.

(5) Only includes nonproportional reinsurance, an arrangement in which a reinsurer makes payments to an insurer whose losses exceed a predetermined amount.

(6) Coverages protecting against legal liability resulting from negligence, carelessness, or failure to act.

Source: SNL Financial LC.

(1) HECMs are federally insured reverse mortgage products.

(2) Through July 2009; fiscal year ends September 30.

Source: National Reverse Mortgage Lenders Association.

(Percent)

Source: U.S. Department of Commerce, Census Bureau; U.S. Department of Housing and Urban Development, Office of Policy Development and Research.

($ billions)

(1) Estimated.

Source: BISRA (formerly Kehrer-LIMRA).

(Percent)

Source: U.S. Department of Commerce, Census Bureau; U.S. Department of Housing and Urban Development, Office of Policy Development and Research.

Source: SNL Financial LC.

Source: U.S. Department of Commerce, Census Bureau, Census of Housing.

(Based on first year collected premium)

(1) Includes career, multiline exclusive and home service agents.

(2) Includes brokers and personal producing general agents.

(3) No producers are involved. Does not include direct marketing efforts involving agents.

(4) Includes stockbrokers, financial institutions, worksite and other channels.

(5) Estimate.

Source: LIMRA’s U.S. Individual Life Insurance Sales Survey and LIMRA estimates.

Source: National Association of Insurance Commissioners (NAIC) Annual Statement Database, via Highline Data, LLC. Copyrighted information. No portion of this work may be copied or redistributed without the express written permission of Highline Data, LLC.

(1) Short-term and long-term disability.

Source: Eastbridge Consulting Group, Inc.

($ billions)

(1) Data for 2009 and 2010 are estimated.

Source: Celent.

(1) Based on an August 2012 survey of 1,000 Americans age 18 and over.

Source: American Bankers Association.

($ billions, net premiums written)

Source: SNL Financial LC.

Source: National Association of Insurance Commissioners (NAIC) Annual Statement Database, via Highline Data, LLC. Copyrighted information. No portion of this work may be copied or redistributed without the express written permission of Highline Data, LLC.

Source: SNL Financial LC.

($ billions, net premiums written)

Source: National Association of Insurance Commissioners (NAIC) Annual Statement Database, via Highline Data, LLC. Copyrighted information. No portion of this work may be copied or redistributed without the express written permission of Highline Data, LLC.