INSURANCE INFORMATION INSTITUTE Florida Press Office: (813) 480-6446, lynnem@iii.org

New York Press Office: (212) 346-5500, media@iii.org

TAMPA, FL, January 26, 2011 — Staged auto accidents and excessive and often unnecessary medical treatment are adding around $1 billion to the costs of Florida’s no-fault auto insurance system, according to an analysis by the Insurance Information Institute (I.I.I.).

The I.I.I. reported that the typical two-car family could be paying what amounts to a “fraud tax” of nearly $100 based on estimated fraud inherent in the state’s current “no-fault” auto insurance system. Multiplied by Florida’s 11,288 million insured vehicles, it means that fraud costs related to no-fault auto insurance could rise to nearly $1 billion by the end of 2011.

The I.I.I.’s white paper, No-Fault Auto Insurance In Florida, illustrates how the number and cost of automobile insurance claims is rising, despite a drop in reported car crashes and safer cars.

“There are more auto insurance claims and a higher percentage of them seem to require extensive medical treatment,” said Lynne McChristian, Florida’s representative for the I.I.I. “This is a costly combination that only offers one reasonable explanation—fraud and abuse of the no-fault auto insurance system is being paid for by all drivers, and steps must be taken to reverse this course.”

The I.I.I. white paper said that no-fault fraud has already cost Florida vehicle owners and their insurers an estimated $853 million since 2008. The cumulative costs from 2009 through 2011 could exceed $1.5 billion, if current trends continue.

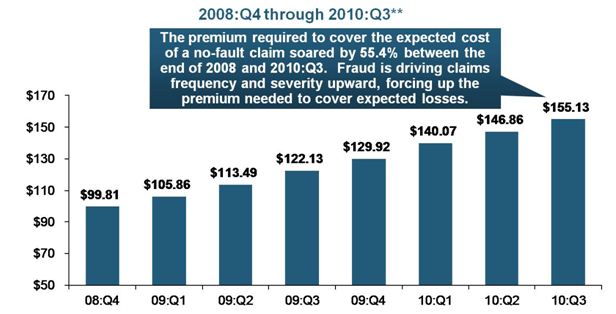

The amount of pure premium required to cover the expected costs of Florida’s no-fault auto system, also known as Personal Injury Protection (PIP), soared 55.4 percent between 2008 and the third quarter of 2010. Pure premium is defined as the amount required to pay only expected losses. It does not include expenses and other costs of doing business.

In the fourth quarter of 2008, the pure premium to cover expected losses was $99.81; By the third quarter of 2010, the amount of pure premium necessary to pay expected losses had soared to $155.13.

FLORIDA NO-FAULT (PIP) PURE PREMIUMS ARE TRENDING SHARPLY UPWARD*

Source: ISO/PCI Fast Track data; Insurance Information Institute.

“The only logical explanation for such a dramatic increase in the expected costs of a no-fault claim is a surge in fraud and abuse, McChristian said.

Florida leads the nations in the number of staged accidents, and staged accidents often lead to treatment for injuries that are nonexistent or greatly exaggerated, enabling unscrupulous medical providers and attorneys to tap into the $10,000 minimum PIP coverage requirement, according to the National Insurance Crime Bureau. (NICB).

Florida is one of 12 states, along with Puerto Rico, that has a no-fault law; the terms PIP and no-fault are used interchangeably to denote any auto insurance program that allows policyholders to recover a financial loss from their own insurer.

Law enforcement has stepped up its investigation of staged scams, which is leading to more arrests and more attention being focused on the criminals who are operating fraud rings.Florida has a Division of Insurance Fraud within the Florida Department of Financial Services (DFS) that helps safeguard citizens against acts of insurance fraud. The DFS offers a reward of up to $25,000 for information leading to the arrest and conviction of people who commit complex, organized insurance crimes.

The National Insurance Crime Bureau (NICB), a nonprofit that receives support from more than 1,000 property and casualty insurers, also has a fraud report line: 800-TEL-NICB. The NICB also has a tip line for cellphones, which can be accessed by texting the keyword “FRAUD” to TIP411 (847411).

THE I.I.I. IS A NONPROFIT, COMMUNICATIONS ORGANIZATION SUPPORTED BY THE INSURANCE INDUSTRY.

Insurance Information Institute, 4775 E. Fowler Avenue, Tampa, FL 33617, (813) 480-6446 | www.insuringflorida.org| www.iii.org