MEMBERSHIP

AMPLIFY

EN ESPAÑOL

Connect With Us

- Popular search terms

- Automobile

- Home + Renters

- Claims

- Fraud

- Hurricane

- Popular Topics

- Automobile

- Home + Renters

- The Basics

- Disaster + Preparation

- Life Insurance

Legal system abuse is a pervasive problem in the United States, with far—reaching implications for consumers and companies. It occurs when some people use the legal system in unscrupulous ways—for their own personal (often monetary) gain rather than for the fair resolution of disputes. Sometimes these activities involve using legal loopholes and sometimes they involve direct fraud. Nonetheless, this behavior can lead to higher costs for insurers and for policyholders in the form of increased insurance premiums and fewer coverage options.

One specific type of legal system abuse is legalized fraud, often caused by tactics such as misusing assignment of benefits (AOB) agreements. An AOB is a legal agreement allowing your insurer to directly pay a third party on your behalf for services provided. For homeowners, auto, and other types of property insurance, the third party, for example, could be a contractor, auto repair shop, or other repair provider. The AOB can expedite the recovery process after an incident, enabling policyholders to move forward with rebuilding their property and lives without unnecessary delays.

However, some third parties exploit these agreements using loopholes in the law and take control of a policyholder's insurance claim. Seizing the opportunity to exaggerate or falsify claims, they may file specious lawsuits. The resulting inflation of claims expenses and unnecessary litigation costs insurers billions annually.

In Florida, fraud and legal abuse shenanigans like these have wreaked havoc on insurance markets for several years. The situation worsens, threatening coverage affordability and availability for state residents.

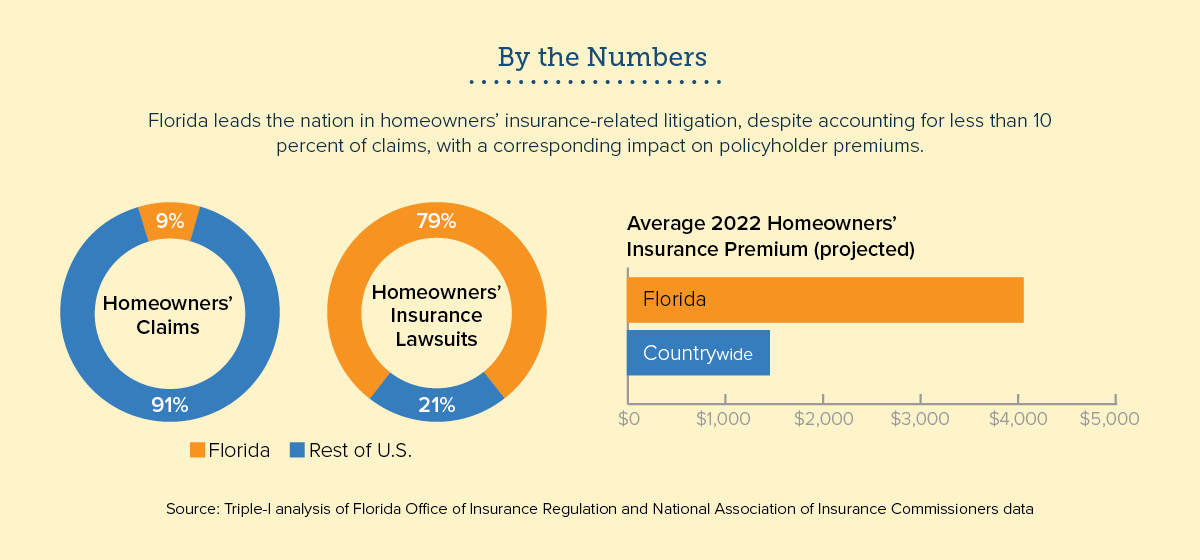

While Florida has long been known for its low taxes and pleasant climate, soaring property insurance premiums are making it increasingly difficult for people to afford homeownership. According to our research, Florida has the highest average property insurance premiums in the nation— $4,231 per year, nearly triple the national average, according to a 2022 Triple-I estimate.

This problem has been exacerbated by irresponsible litigation practices, such as law firms filing thousands of lawsuits based on contractor fraud schemes. Litigation abuse has been fueled by a lack of transparency and ballooning costs due to fraudulent claims—leading to large paydays for trial attorneys at the expense of insurers and policyholders. Many insurers have reluctantly agreed to large settlements to avoid court-awarded fees, and, in turn, raised premiums to cover legal costs and other risks. As a result, the average Florida homeowner has seen their rates increase by a cumulative 50% or more over the last two years.

According to Triple-I's Mark Friedlander, premiums are only expected to escalate with an estimated 40% average statewide rate increase projected in 2023 for customers of private insurers.

As a result, the number of policies with Citizens Property Insurance Corp., the state-backed insurer of last resort, has skyrocketed, increasing by 50% in 2002. However, as Citizens is not allowed to charge actuarially-sound rates, it risks undercutting and weakening a private market already overburdened with rising claims costs. Analysts are also concerned that policyholders across the state could get hit with extra fees — referred to as assessments — if the insurer can't pay all its claims should an immensely damaging hurricane or series of hurricanes strike.

Further, real estate experts have expressed concerns about the detrimental impact of the insurance crisis on the state's booming housing market. Some new home buyers have struggled to find affordable property insurance coverage or simply coverage at all––increasing trends that could create economic downturns for the state. Florida's coverage affordability and accessibility situation has been mounting for years but is growing more precarious for residents and insurers alike.

Insurers are also struggling with growing losses due to catastrophes and rising reinsurance costs. Underwriting losses have exceeded $1 billion in each of the last three years (2020-2022).

It's no surprise that seven Florida-domiciled residential insurers failed since February 2022 while many others have either pulled out of the market entirely or stopped writing new business because they can't cover their risks. This trend has accelerated recently as AOB claims account for 9% of all insured loss costs — almost double what it was in 2013 - adding an extra $675 million in costs statewide every year since 2017 according to one estimate.

The situation is so serious that the Florida Office of Insurance Regulation has 24 insurers on its 2023 financial watchlist for potential insolvency due primarily to high levels of litigation expenses.

With insurance market destabilization posing a clear threat to the public, lawmakers have steadily taken steps to address the problem before it spirals out of control.

Florida legislators passed substantial property insurance reforms in December 2022 to stabilize the insurance market for homeowners and protect them from rampant AOB fraud.

The new law eliminates legal fee structures that allowed AOB abusers to skirt the justice system and forced insurers to pay inflated claims to unscrupulous third parties directly for thousands of questionable claims. This change incentivizes both insurers and contractors to be more transparent with pricing so they will have an easier time communicating with one another without fear of legal retribution.

Additionally, the legislation sets up mechanisms that allow policyholders to dispute any costs they deem unfair before a claim is paid out - something they could not do under previous laws.

By addressing the root cause of Florida’s man-made insurance crisis through these substantial reforms, state lawmakers have taken a major step toward stabilizing the market for homeowners by protecting them from AOB fraudsters who would take advantage of them through regulatory loopholes.

Further tort reform enacted in the Florida Legislature’s regular session in March 2023 will reduce attorney fee multipliers that courts have been liberally awarding on top of plaintiff verdicts in property claim lawsuits and will also benefit other lines of personal and commercial insurance.

The legislative progress is just the beginning, however, as more regional residential insurers are still at risk of failure this year due to excessive litigation expenses and efforts are underway to undo or work around the new statutes.

Florida’s leaders must fight any efforts to erode the impacts of the recent reform package.

Fraudsters rely on regulatory loopholes (that have been upheld by multiple court rulings) to cash in on billions of dollars from abusive lawsuits. Lawmakers must ensure that reforms are implemented in the strongest feasible way absent of loopholes that would allow the problem to continue. Several plaintiffs’ firms have filed lawsuits by the thousands, with one being sanctioned for its unethical practices by the Florida Supreme Court.

Florida has a serious challenge ahead in tackling legal system abuse, and Triple-I has resources that can help inform the solutions. As these factors further increase financial pressure on claims payers, it's critical for insurers and policyholders alike to stay updated on reform efforts such as this latest legislation implemented by Florida’s Legislature.

By understanding the impacts of AOB fraud on their bottom line, insurers may be able to create tailored strategies toward proactive risk management specifically geared toward counteracting socially inflated lawsuit settlements. We need to inform consumers and constituents that legalized fraud is weighing on their insurance bills and their ability to have insurance at all.

Triple-I stands ready to serve as a resource to inform the decision and help lead Florida’s property insurance market toward greater stability.

Social inflation: hard to measure, important to understand

Florida Issue: Brief Homeowner insurance Crisis

Florida Issue: Brief Addressing State Insurance Crisis

Social inflation with Sean featuring Florida.

Social inflation impact on consumers.

Triple-I: Extreme Fraud and Litigation Causing Florida's Homeowners Insurance Markets Demise