MEMBERSHIP

AMPLIFY

EN ESPAÑOL

Connect With Us

- Popular search terms

- Automobile

- Home + Renters

- Claims

- Fraud

- Hurricane

- Popular Topics

- Automobile

- Home + Renters

- The Basics

- Disaster + Preparation

- Life Insurance

FOR IMMEDIATE RELEASE

New York Press Office: (212) 346-5500; media@iii.org

Florida Press Office: (813) 480-6446; lynnem@iii.org

NEW YORK, August 11, 2017 — Hurricane Andrew struck Florida on August 24, 1992, and the upheaval the Category 5 storm created for the property insurance market remains a reminder of the necessity of managing risk and striving for resiliency in the nation’s most disaster-prone state, according to the Insurance Information Institute (I.I.I.).

Among those lessons was an awakening to Florida’s exposure to catastrophic loss. “Prior to that August day in 1992, few had come to grips with the necessity of being both financially and structurally resilient,” said Sean Kevelighan, CEO, I.I.I. “Financial resiliency means getting the right type and amount of insurance. And, being structurally resilient means building above the current building code standards with structures tough enough to withstand major storms.”

Andrew ushered in several key lessons that still resonate today, which have changed the way the insurance market works, not only in Florida but in all coastal states, said the I.I.I. These enduring lessons affect the way insurers approach the marketplace and the way in which they manage coastal risk:

Hurricane deductibles exist in 19 states and the District of Columbia. These are percentage deductibles that help maintain the availability and affordability of insurance. With these deductibles in place, insurers are able to purchase reinsurance (which is insurance for insurance companies) at a lower cost, which also helps keep premiums in check.

Florida law requires insurers to inform policyholders of the exact dollar amount of their hurricane deductible, which for most people is a percentage of the insured value of their home. The I.I.I. suggests that policyholders review their insurance policy in advance to know the amount of hurricane risk they share.

“You can find the exact dollar amount of the hurricane deductible on the declarations page of a homeowners insurance policy,” said Lynne McChristian, Florida spokesperson for the I.I.I. “Knowing that amount is the first step in planning for the out-of-pockets costs that come with."

3. Spreading Florida’s risk globally and the growth of domestic insurers

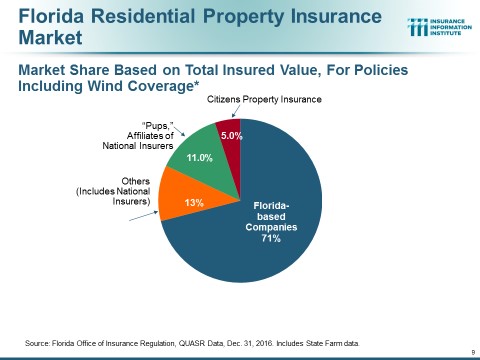

The severity of the losses from Andrew caused insurers to take unprecedented steps to reduce their future risk exposure. Those steps ranged from nonrenewal or cancellation of policies to requests for significant rate increases. As national insurers retreated, the market transitioned to new entrants forming Florida companies, a trend made possible by access to reinsurance.

Insurance companies buy reinsurance for a number of reasons, and almost all reinsure at least some of their risk. Reinsurance spreads risk in a way insurers cannot do alone. With this backup capital for paying claims, insurers are able to write more direct business. Global reinsurance capital reached a new high in 2017, with more opportunities for trading risk. This adds to the stability of the marketplace and enables insurers to pay claims quickly.

Florida has a mandatory public catastrophe mechanism, the Florida Hurricane Catastrophe Fund (FHCF), from which all insurers operating in the state must buy reinsurance. However, this fund is not designed to pay for all layers or all types of losses from natural disasters. Buying reinsurance from multiple sources spreads risk, and there is ample capacity in the global financial market to meet the demand for this protection.

4. Managing and minimizing government roles in insurance

The difference between private insurers and state-run entities is that private companies must have the money needed to pay claims in advance, while state-run companies can run deficits and tax all policyholders in the state to make up for losses. Like the FHCF, Citizens Property Insurance is another state-run entity. Its exposure grew exponentially following Hurricane Andrew, and it continued to grow as private insurers curtailed the amount of business they could take on. Aggressive efforts to depopulate Citizens have succeeded in reducing its exposure, with the company now half its peak size in terms of policy count. This is a positive outcome since the threat of risk assessments on all policyholders is greatly reduced. Additionally, Citizens has taken proactive steps to minimize deficits by purchasing reinsurance and catastrophe bonds (another innovative risk transfer product) to further reduce the likelihood of deficits following a major hurricane.

“There hasn’t been a major hurricane in Florida in a dozen years,” said McChristian. “As a result, many people have ‘hurricane amnesia’ or have never experienced the devastation; they just aren’t prepared. Remembering the lessons from Hurricane Andrew is essential to being able to bounce back from the next major storm.”

RELATED LINKS

Hurricane Season Insurance Checklist

Understanding Your Insurance Deductible

Facts and Statistics: Hurricanes White Paper: Hurricane Andrew and Insurance: The Enduring Impact of an Historic Storm (2012)

The I.I.I. has a full library of educational videos on its You Tube Channel. Information about I.I.I. mobile apps can be found here.

THE I.I.I. IS A NONPROFIT, COMMUNICATIONS ORGANIZATION SUPPORTED BY THE INSURANCE INDUSTRY.

Insurance Information Institute, 110 William Street, New York, NY 10038